This week, NIC MAP® Data Service clients attended a webinar on the seniors housing market trends during the first quarter of 2017. Key takeaways included:

-

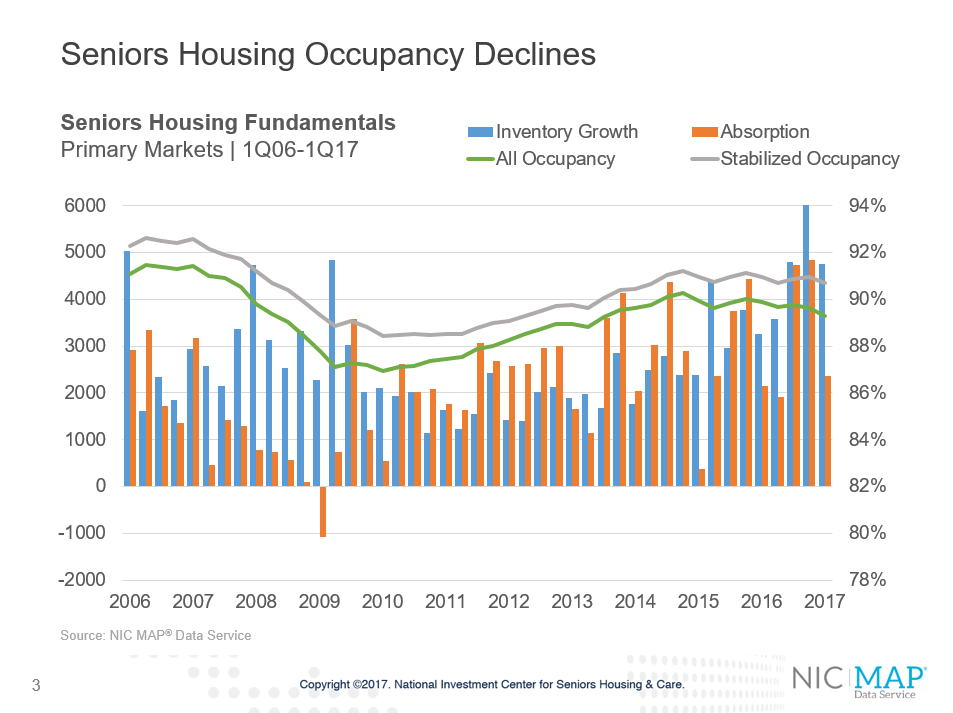

Takeaway #1: Occupancy Fell in the First Quarter

- The occupancy rate for seniors housing properties fell 30 basis points in the first quarter of 2017 to 89.3%, as net additions to inventory outpaced absorption of units. This placed it 240 basis points above its cyclical low of 86.9% during the first quarter of 2010 and 90 basis points below its most recent high of 90.2% in the fourth quarter of 2014. The occupancy rates for independent living properties and assisted living properties continue to diverge, with independent living recording a relatively strong 90.9% occupancy rate, while the rate for assisted living fell 50 basis points to 87.2%. The occupancy rate for assisted living was at its lowest level since early 2010 when it stood at 86.9%.

-

Takeaway #2: Some of the First Quarter Drop in Occupancy in Assisted Living Was Seasonal

- First quarter occupancy rates often retreat somewhat due to the effects of weather and the flu season on move-in and move-out rates. Using a statistical method, some of this seasonality can be accounted for and the drop in occupancy is less severe. On a seasonally-adjusted basis, assisted living stabilized occupancy fell a lesser 30 basis points to 89.5% from 89.8% in the fourth quarter. This compares with a 60 basis point decline on a non-adjusted basis to 89.4% from 90.0% for the stabilized assisted living occupancy rate.

-

Takeaway #3: Annual Inventory Growth Outpacing Annual Absorption

- Inventory growth continues to outpace demand, causing the occupancy rate to decline. For independent living properties, the pace of inventory growth has been accelerating since early 2015, following several years of relatively flat growth. Meanwhile, the rate of absorption has been accelerating also since mid-2016 and as of the first quarter, inventory growth exceeded absorption by 20 basis points—2.3% versus 2.1%. That made the annual absorption rate the highest since late 2014 and the inventory growth rate the highest since early 2010.

- For assisted living, inventory growth has been ramping up for a much longer period than has independent living and as of the first quarter, annual inventory growth reached its highest level since NIC began collecting the data—4.9%. As the graph shows, annual absorption has flattened out for the last several quarters and came in at a 3.7% pace in the first quarter of 2017. This made the gap between inventory growth and absorption the widest it has been since 2009.

-

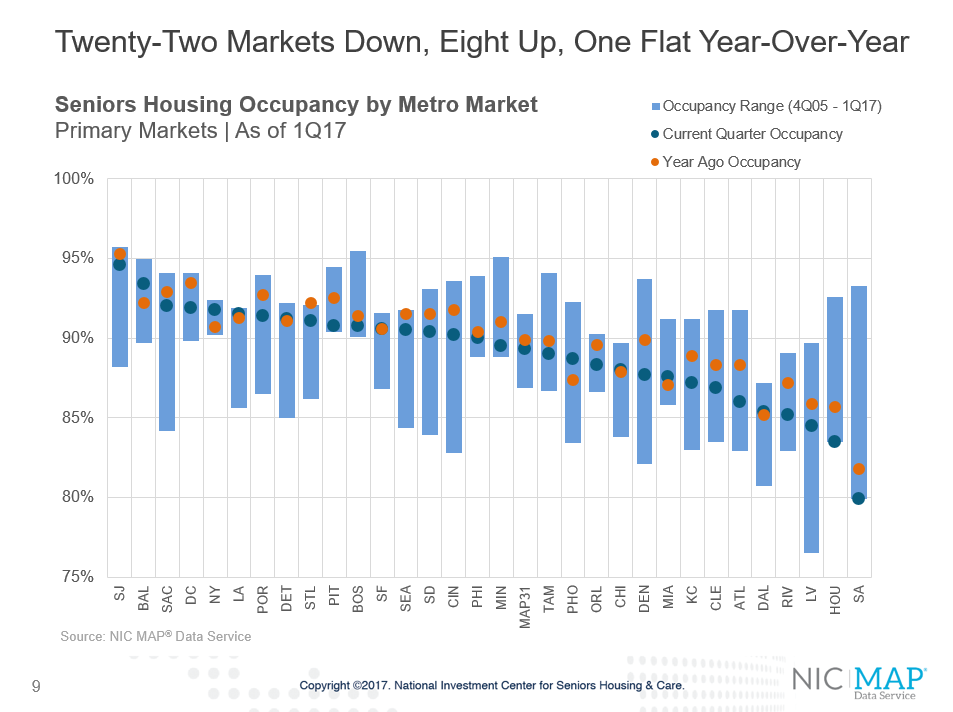

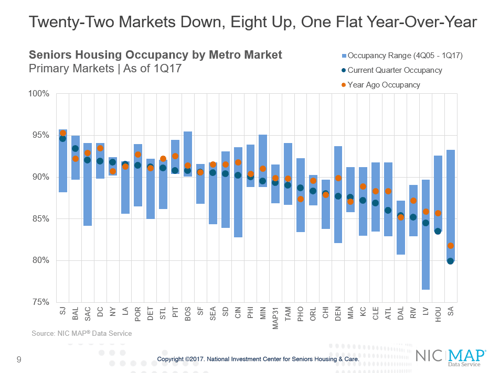

Takeaway #4: Market Variation is Great

- At the metropolitan area level, occupancy rates vary greatly as different trends in supply and demand impact performance. In the first quarter, occupancy rates ranged from 79.0% in San Antonio to 94.6% in San Jose. This compares to the Primary Market average of 89.3%. Markets that added significant levels of new inventory in the past year include Dallas, Minneapolis, Atlanta, Chicago, Houston, New York and Boston.

-

Takeaway #5: Same-Store Rent Growth Remains Strong

- Same-store asking rent growth for seniors housing decelerated, but remained generally strong in the first quarter, with year-over-year growth of 3.3%. This was down from 3.7% in the fourth quarter, but was up from 3.1% in the first quarter of 2016.

- Asking rent growth for assisted living was 3.0% for the first quarter, down 30 basis points from the fourth quarter. For independent living, rent growth decelerated to 3.5% from 4.0% in the fourth quarter and down from 4.2% in the third quarter, when rent growth reached its highest pace since NIC began collecting this data.

- There is wide variation in rent growth, however, with Orlando and Miami experiencing seniors housing rent growth of 1% or less, while Saint Louis and Sacramento had growth of nearly 5%.

-

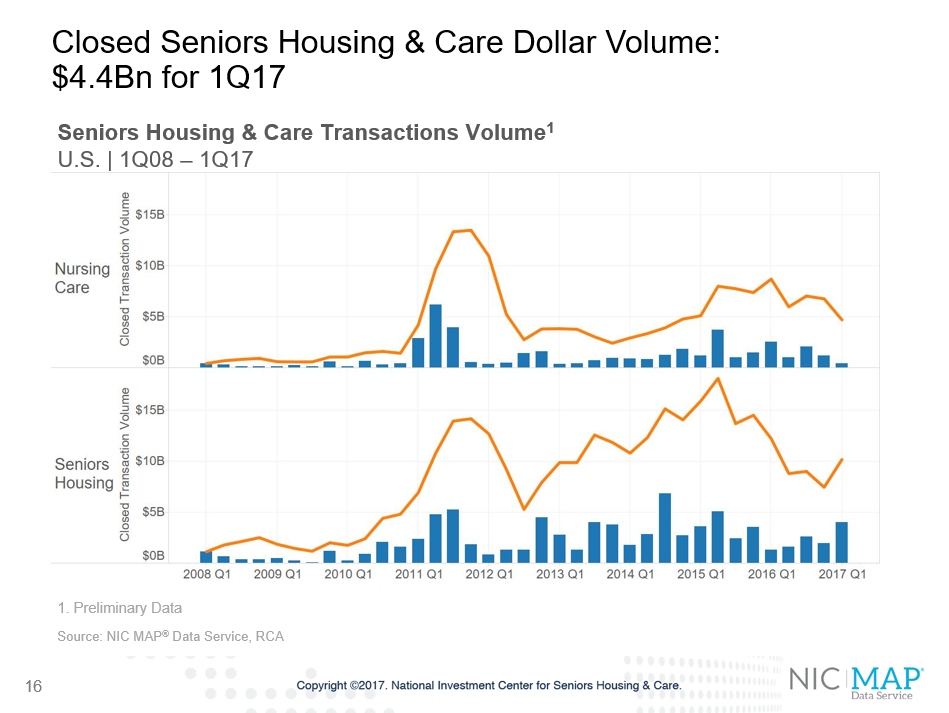

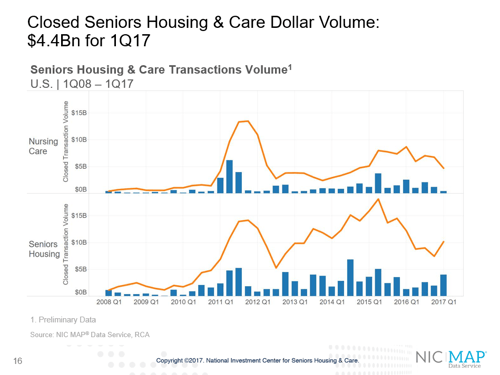

Takeaway #6: Transaction Volume Picks Up

- Seniors housing transaction volume accelerated in the first quarter and totaled $4 billion, up 41% from the fourth quarter. The strong pace stemmed from a few large deals. The public buyers’ share of volume continued to decrease, while institutional buyers share increased. Skilled nursing transactions slowed to $400 million in the first quarter.

About Beth Mace

Beth Burnham Mace is a special advisor to the National Investment Center for Seniors Housing & Care (NIC) focused exclusively on monitoring and reporting changes in capital markets impacting senior housing and care investments and operations. Mace served as Chief Economist and Director of Research and Analytics during her nine-year tenure on NIC’s leadership team. Before joining the NIC staff in 2014, Mace served on the NIC Board of Directors and chaired its Research Committee. She was also a director at AEW Capital Management and worked in the AEW Research Group for 17 years. Prior to joining AEW, Mace spent 10 years at Standard & Poor’s DRI/McGraw-Hill as director of its Regional Information Service. She also worked as a regional economist at Crocker Bank, and for the National Commission on Air Quality, the Brookings Institution, and Boston Edison. Mace is currently a member of the Institutional Real Estate Americas Editorial Advisory Board. In 2020, Mace was inducted into the McKnight’s Women of Distinction Hall of Honor. In 2014, she was appointed a fellow at the Homer Hoyt Institute and was awarded the title of a “Woman of Influence” in commercial real estate by Real Estate Forum Magazine and Globe Street. Mace earned an undergraduate degree from Mount Holyoke College and a master’s degree from the University of California. She also earned a Certified Business Economist™ designation from the National Association of Business Economists.

Connect with Beth Mace

Read More by Beth Mace