A NIC report developed to provide timely insights from owners and C-suite operators on the pulse of seniors housing and skilled nursing sectors.

This report marks the second installment of findings from NIC’s weekly Executive Survey of operators in seniors housing and skilled nursing. The report highlights the findings from responses collected at the beginning of the pandemic to now as operators experience changing market conditions due to the COVID-19 threat to residents, staff and business operations; effects of social distancing mandates from state and local governments and seniors housing and care organizations themselves; and the economic effects of shuttered non-essential businesses on local economies.

Summary of Insights and Findings

- The share of organizations reporting lower occupancy rates from the prior month increased in Wave 2. This directional decline in occupancy rates from the prior month occurred across care segments and are supported by anecdotal reports from operators, with some expecting to see greater impact in the coming weeks.

- The segment with the largest share of operators reporting a decrease in occupancy from the prior month was nursing care, with 70% of respondents noting downward directional trends in occupancy rates in Wave 2. The nursing care segment also saw the largest deceleration of move-ins in the past 30-days, likely driven by fewer hospitals discharging patients to post-acute care settings for rehabilitative therapy as hospitals defer elective surgeries due to the pandemic.

- While the majority of organizations continued to report no change in the pace of move-outs by segment, a larger share of respondents reported an increase in move-outs across the board compared to Wave 1. Additionally, the pace of move-ins has decelerated across all segment types compared to Wave 1, except for memory care. Two-thirds attribute the deceleration in move-ins to a slowdown in leads conversion/sales due to a moratorium on in-person tours to keep residents and staff protected from outside contagion. Additionally, about half have an organization-imposed ban on settling new residents into their communities.

- Workforce shortages and staffing challenges are putting financial stress on some organizations. Most are back-filling staffing shortages by increasing overtime hours, and they are supporting the health and wellbeing of property staff by providing flexible work hours and remote work; some are also offering additional paid sick leave and food and meals support for staff and their families.

- Slightly more respondents in Wave 2 expect no change or a decrease in their development pipeline going forward than in Wave 1. While several respondents have new development and/or expansion plans currently underway, uncertainty is a primary concern going forward in the coming weeks and months, despite the prevailing sentiment that demand for seniors housing will continue to grow. This may continue the recent trend seen in NIC MAP data showing a decline in new construction relative to existing supply.

Wave 2 Survey Demographics

- Responses were collected April 1-12, 2020 from owners and C-suite executives of 146 seniors housing and skilled nursing operators from across the nation.

- 59% of respondents were exclusively for-profit providers, 31% were exclusively nonprofit providers, and 10% operate both for-profit and nonprofit seniors housing and care organizations.

- Owner/operators with 1 to 10 properties comprise 61% of the sample. Operators with 11 to 25 properties make up 21% while operators with 26 properties or more make up 18% of the sample.

- Many respondents in the sample report operating combinations of property types. Across their entire portfolios of properties, 75% of the organizations operate seniors housing properties (IL, AL, MC), 34% operate CCRCs (Life Plan Communities), and 32% operate nursing care properties.

Key Survey Results

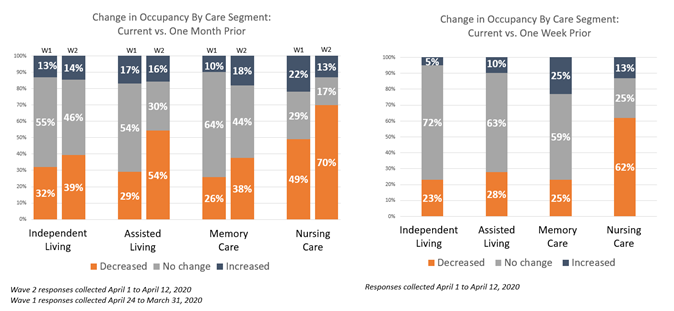

Change in Occupancy by Care Segment

Respondents were asked: “Considering the entire portfolio of properties, overall, my organization’s occupancy rates by care segment are… (Most Recent Occupancy, Occupancy One Month Ago, Occupancy One Week Ago, Percent 0-100)”

- Approximately one-third to one half of organizations reporting on their independent living, assisted living and memory care units in Wave 2—across their respective portfolios of properties—saw a decrease in occupancy from the prior month. Roughly one fourth saw a decrease compared with the prior week. There were more survey respondents reporting a decrease in occupancy in Wave 2 results than in Wave 1 results.

- Conversely, roughly half to two-thirds of organizations reporting on their independent living, assisted living and memory care units in Wave 2 saw no change or an increase in occupancy rates from the time they responded April 1-April 12, 2020 to one month prior; down from roughly two-thirds to three-quarters in Wave 1.

- Organizations with nursing care beds reported the largest directional declines in occupancy among the four segment types and more respondents reported declines in Wave 2 than in Wave 1. Nearly three-quarters to half of organizations with nursing care beds and assisted living units reported occupancy declines in Wave 2.

- Compared to one week prior, most organizations report little change in occupancy by care segment, except nearly two-thirds of organizations saw occupancy declines in nursing care beds from a week ago, and a quarter saw occupancy increases in memory care units.

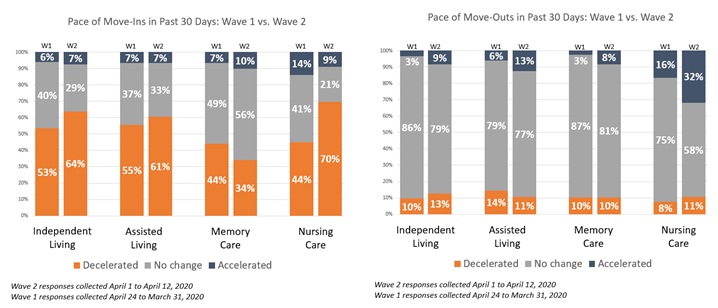

Pace of Move-Ins and Move-Outs

Respondents were asked: “Considering my organization’s entire portfolio of properties, overall, the pace of move-ins and move-outs by care segment in the past 30-days has…”

- Generally, more organizations in the recent Wave 2 survey than in Wave 1 report that the pace of move-in rates decelerated over the past 30-days. Approximately two-thirds to three-quarters report a deceleration in move-ins. Only one-third of organizations reporting on their memory care units noted a deceleration.

- The majority of respondents noted no change in move-outs, with generally slight declines from Wave 1 to Wave 2.Nursing care beds had a higher pace of accelerated move-outs compared to other care segments in Wave 2.

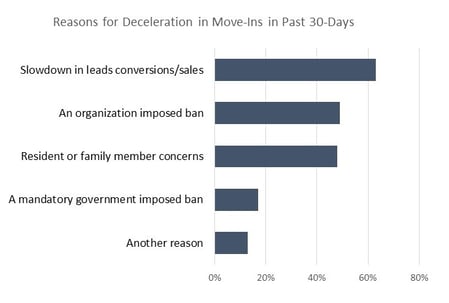

- About two-thirds to one half of respondents attributed the deceleration in move-ins to a slowdown in leads conversion/sales, an organization-imposed ban and/or resident or family member concerns. At this point in the pandemic, fewer than a quarter of organizations attribute a deceleration in move-ins to a mandatory government ban.

Mitigation Strategies for Labor Shortages

Respondents were asked: “My organization is back-filling property staffing shortages by utilizing… (Choose all that apply)”

- Consistent with Wave 1, organizations in Wave 2 are:

- increasing overtime hours (89%)

- hiring agency or temp staff (43%)

- hiring professionals from other industries (29%)

- using volunteers (14%)

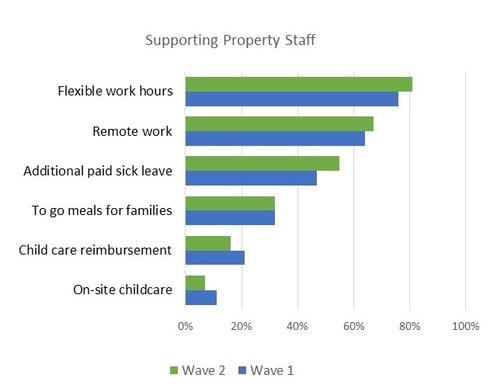

Supporting Property Staff

Respondents were asked: “My organization is supporting property staff who may be experiencing challenges by providing… (Choose all that apply)”

- Most respondents in Wave 2 and Wave 1 report offering flexible work hours and remote work. Others provide additional paid sick leave and to-go meals for families; some are addressing challenges by providing staff childcare.

Development Pipeline Considerations

Respondents were asked: “My organization’s projected development pipeline going forward is expected to… (Choose all that apply)”

- There are generally minimal differences in expectations about organizations’ development pipelines between Wave 2 and Wave 1, however slightly more respondents expect no change (46% vs. 42%) or a decrease (35% vs 25%).

- Uncertainty (95% vs. 88%), and lack of construction labor (13% vs. 3%) between Wave 2 and Wave 1 appear to be growing concerns. Like Wave 1, about 20% in Wave 2 cite supply chain disruptions.

NIC wishes to thank survey respondents for their valuable input and continuing support for this effort to bring clarity and transparency into market fundamentals in the seniors housing and care space at a time where trends are rapidly changing. Your support helps provide both capital providers and capital seekers with data as to how COVID-19 is impacting the space, helping leaders make informed decisions.

If you are an owner or C-suite executive of seniors housing and care properties and have not received an email initiation but would like to participate in the current Executive Survey, please click here for the online questionnaire.

About Lana Peck

Lana Peck, former senior principal at the National Investment Center for Seniors Housing & Care (NIC), is a seniors housing market intelligence research professional with expertise in voice of customer analytics, product pricing and development, market segmentation, and market feasibility studies including demand analyses of greenfield developments, expansions, repositionings, and acquisition projects across the nation. Prior to joining NIC, Lana worked as director of research responsible for designing and executing seniors housing research for both for-profit and nonprofit communities, systems and national senior living trade organizations. Lana’s prior experience also includes more than a decade as senior market research analyst with one of the largest senior living owner-operators in the country. She holds a Master of Science, Business Management, a Master of Family and Consumer Sciences, Gerontology, and a professional certificate in Real Estate Finance and Development from Massachusetts Institute of Technology (MIT).

Connect with Lana Peck

Read More by Lana Peck