Insights in Seniors Housing & Care

By: Lana Peck | May 28, 2020

COVID-19 | Executive Survey Insights | Market Trends | Senior Housing | Skilled Nursing

A NIC report developed to provide timely insights from owners and C-suite operators and executives on the pulse of seniors housing and skilled nursing sectors.

NIC’s weekly Executive Survey of operators in seniors housing and skilled nursing is designed to deliver transparency into market fundamentals in the seniors housing and care space at a time where market conditions are rapidly changing—providing both capital providers and capital seekers with data as to how COVID-19 is impacting the space, helping leaders make informed decisions.

This week’s sample (Wave 7) includes responses collected May 11-May 24, 2020 from owners and executives of 155 seniors housing and skilled nursing operators from across the nation. Detailed reports for each “wave” of the survey can be found on the NIC COVID-19 Resource Center webpage under Executive Survey Insights.

Join other operators in the sector and participate in the next wave.

Summary of Insights and Findings

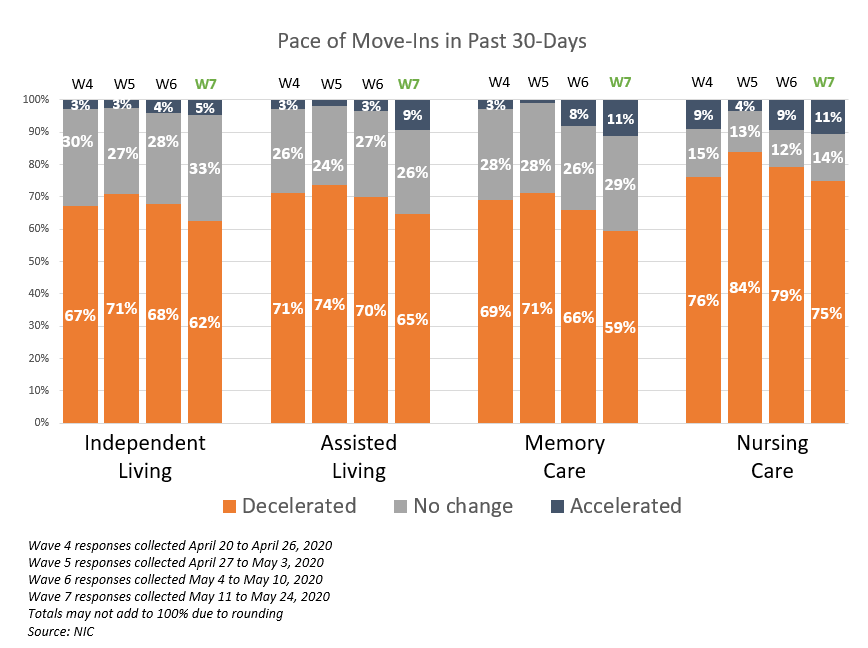

While most organizations continue to report a deceleration in move-ins in the past 30-days, in Wave 7 of the survey, the shares of organizations reporting deceleration is the lowest—across each of the care segments—since the first two waves of the survey (data collected March 24-31 and April 1-12).

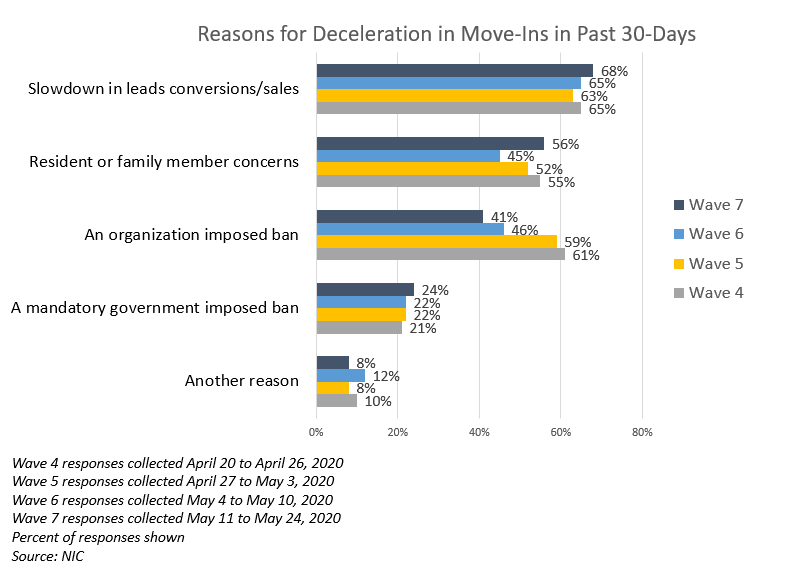

Reasons cited for a deceleration in move-ins continue to primarily be slow leads conversions/sales resulting in difficulty replacing residents who have passed away or moved out; however, about 20% fewer organizations cite an organization-imposed ban on move-ins in Wave 7 compared to Wave 4, as all of the states in the country have begun to loosen social and economic restrictions. About one-half of respondents continue to cite resident or family member concerns about moving in. Others note fewer hospital referrals and elective surgeries, and general concerns about the economy.

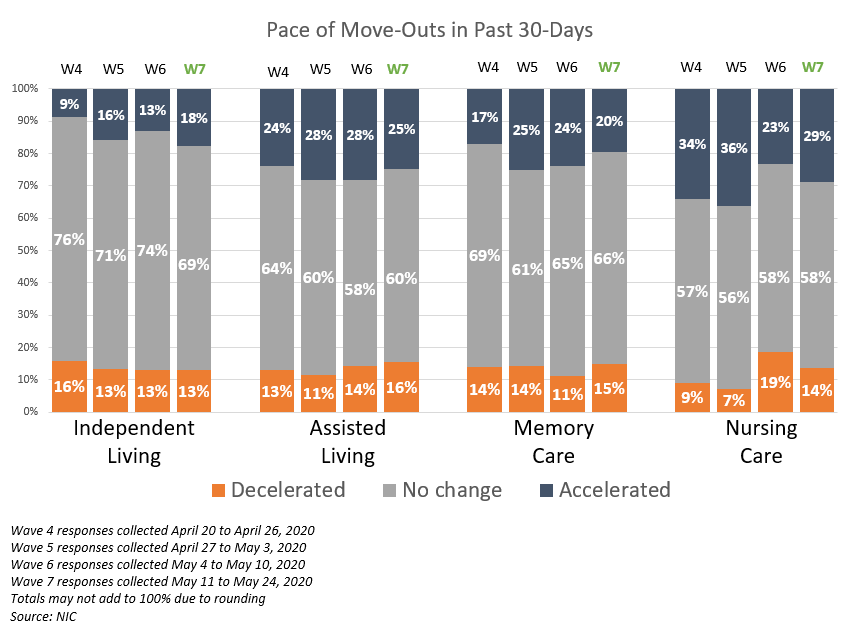

Most organizations continue to report no change in the pace of move-outs in the past 30-days. Of those that did experience an acceleration in the pace of move-outs, reasons cited include a growing percentage of residents transferring to higher levels of care. Other respondents cited nonspecific resident deaths and hospitalizations, resident or family member concerns and normal discharges.

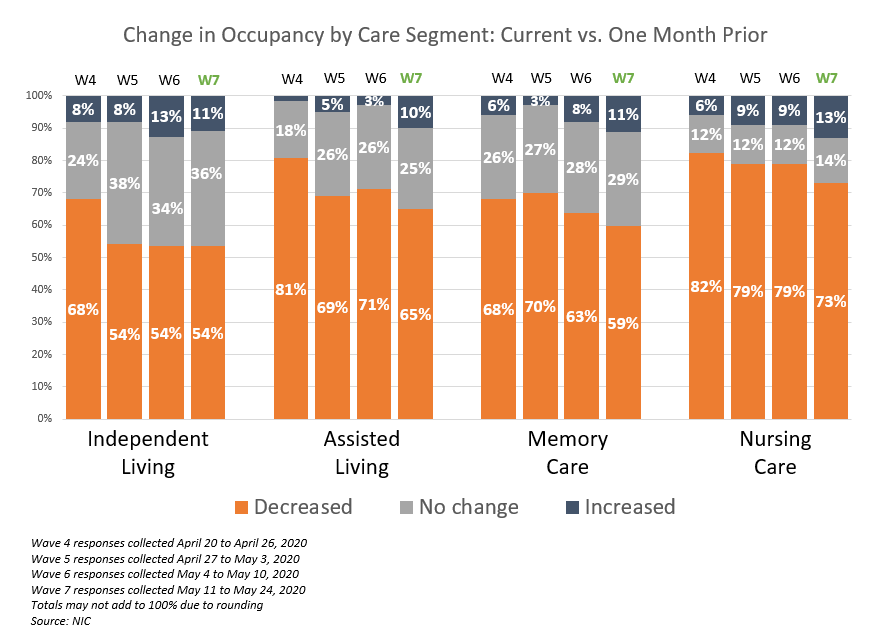

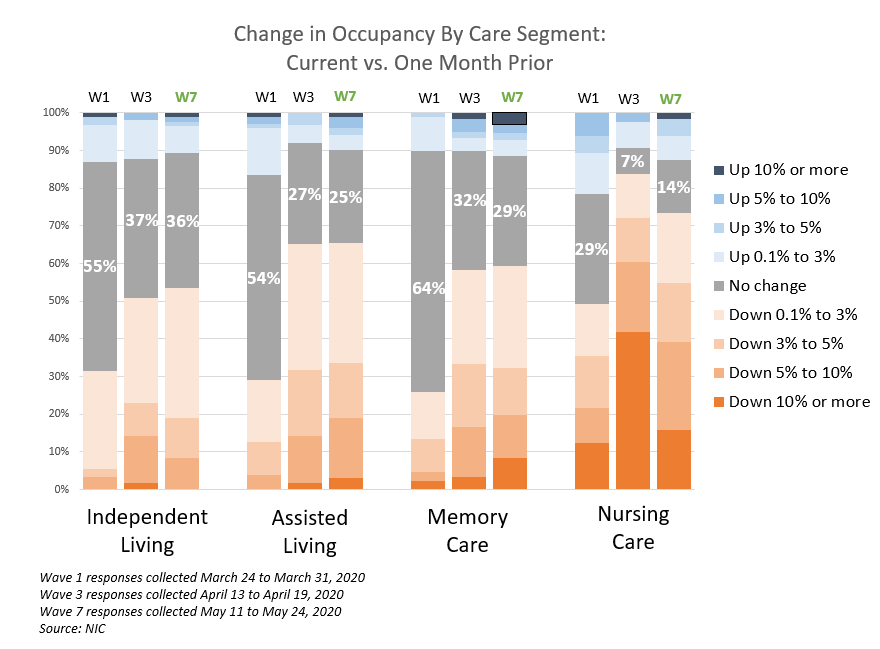

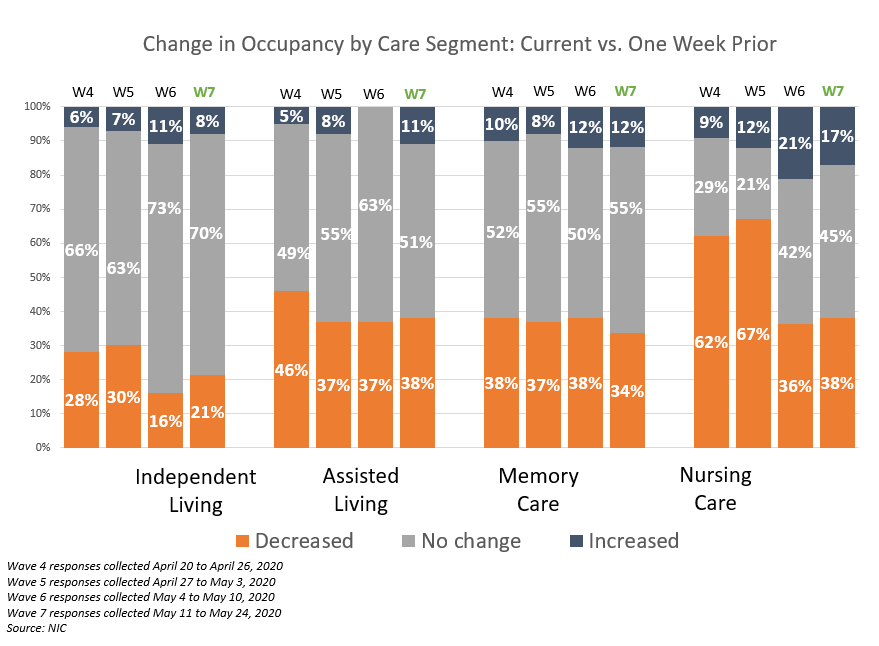

Fewer organizations saw a decrease in occupancy compared to earlier survey waves. Respondents with assisted living and memory care segment units report slightly higher shares of stable or improving occupancy rates from a week ago. And, just over one-third of the organizations reporting on their nursing care segments, in two consecutive waves of the survey, note occupancy rate declines from one week prior (38% and 36%)—significantly lower than in Waves 5 and 4 (67% and 62%).

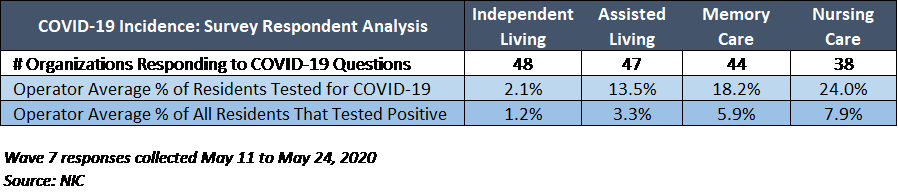

The percentage of residents that were tested for COVID-19 by care segment rose with acuity level. The operator average share of residents tested by segment ranged from 2.1% for independent living, 13.5% for assisted living, 18.2% for memory care and 24.0% for nursing care. These rates of testing are higher than the previous time frame, with the exception of the independent living segment.

Wave 7 Survey Demographics

Key Survey Results

Pace of Move-Ins and Move-Outs

Respondents were asked: “Considering my organization’s entire portfolio of properties, overall, the pace of move-ins and move-outs by care segment in the past 30-days has…”

Reasons for Deceleration in Move-Ins

Respondents were asked: “The deceleration in move-ins is due to…”

Move-Outs

Change in Occupancy by Care Segment

Respondents were asked: “Considering the entire portfolio of properties, overall, my organization’s occupancy rates by care segment are… (Most Recent Occupancy, Occupancy One Month Ago, Occupancy One Week Ago, Percent 0-100)”

Incidence of COVID-19 Among Survey Respondents

Data was collected between May 11 and May 24 (Wave 7) and April 27 and May 10, 2020 (Waves 5 and 6 combined).

Answering on behalf of their organizations, seniors housing and care owners and executives provided the COVID-19 incidence data shown below. The data represents a subsample of the total respondents that answered the COVID-19 questions fully, is self-reported and non-validated, and should not be considered a statistical representation of COVID-19 incidence in seniors housing and care, in general.

NIC wishes to thank survey respondents for their valuable input and continuing support for this effort to bring clarity and transparency into market fundamentals in the seniors housing and care space at a time where trends are rapidly changing. Your support helps provide both capital providers and capital seekers with data as to how COVID-19 is impacting the space, helping leaders make informed decisions.

If you are an owner or C-suite executive of seniors housing and care properties and have not received an email invitation but would like to participate in the current Executive Survey, please click here for the current online questionnaire.

Lana Peck, former senior principal at the National Investment Center for Seniors Housing & Care (NIC), is a seniors housing market intelligence research professional with expertise in voice of customer analytics, product pricing and development, market segmentation, and market feasibility studies including demand analyses of greenfield developments, expansions, repositionings, and acquisition projects across the nation. Prior to joining NIC, Lana worked as director of research responsible for designing and executing seniors housing research for both for-profit and nonprofit communities, systems and national senior living trade organizations. Lana’s prior experience also includes more than a decade as senior market research analyst with one of the largest senior living owner-operators in the country. She holds a Master of Science, Business Management, a Master of Family and Consumer Sciences, Gerontology, and a professional certificate in Real Estate Finance and Development from Massachusetts Institute of Technology (MIT).

Connect with Lana Peck