Insights in Seniors Housing & Care

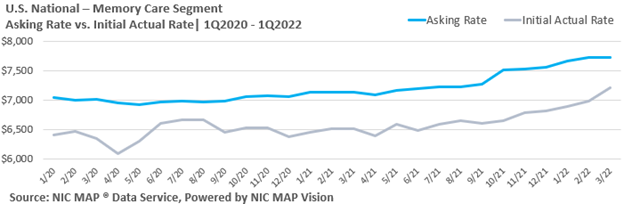

Data from the recently released 1Q2022 NIC MAP Vision Actual Rates Report shows that all three care segments (independent living, assisted living, and memory care) hit the recorded highs in the time series to date for year-over-year growth of asking rates in the first quarter 2022. The report includes monthly data of actual rates and leasing velocity through March 2022, including data on rate discounting and move-in/move-out trends. Read on for further key takeaways from the report produced by NIC MAP® Data Service, powered by NIC MAP Vision.

The first quarter 2022 Actual Rates Report includes segment type data for many more metropolitan markets than were included in previous reports. Prior reports included Atlanta, Philadelphia, and Phoenix, and new metros available in the first quarter 2022 report include Boston, Chicago, and San Diego, among others. NIC MAP Vision continues to work to onboard new data contributors and is dedicated to reporting more metros. It is only with the support of Actual Rates data contributors and officially certified Actual Rates software partners that this expanded reporting is now available. For more information on which metropolitan markets are now available to NIC MAP Vision subscribers, please contact a product expert at NIC MAP Vision today.

Key takeaways from the 1Q2022 NIC MAP Vision Seniors Housing Actual Rates Report are listed below. These key takeaways are from the Segment Type report. Care segments refer to the levels of care and services provided to a resident living in an assisted living, memory care, or independent living unit.

Additional key takeaways are available to NIC MAP Vision subscribers in the full report.

Acknowledging the NIC MAP Vision team. The Actual Rates Data Initiative has been supported by many players behind the scenes over the years, all of whom deserve recognition for their hard work in bringing these data to market. NIC would like to acknowledge and thank Robb Tufts, Dan Mandeville, Raheem Thomas, Aisha Jones, Justin Cassell, Brian Connolly, Rosemary Asquino, Wendy Lazo, Molly McCarter, Leighann Garcia, and Dan Raney of the NIC MAP Vision team for all of their hard work collecting, processing, and reporting the data over the years to achieve this goal of expanding the metro coverage of Actual Rates reporting. Without their continued effort and dedication this increased transparency would not be available to NIC MAP clients.

Arick Morton on the Importance of Actual Rates Data Initiative. Arick Morton, CEO of NIC MAP Vision, discusses the importance of the actual rates data initiative for the company and the senior housing industry at large. Operators can learn more about actual rates by visiting the actual rates page.

The NIC MAP Vision Seniors Housing Actual Rates Report provides aggregate national data from approximately 300,000 units within more than 2,600 properties across the U.S. operated by 25 to 30 senior housing providers. The operators included in the current sample tend to be larger, professionally managed, and investment-grade operators as we currently require participating operators to manage five or more properties. Note that this monthly time series is comprised of end-of-month data for each respective month.

While these trends are certainly interesting aggregated across the states, actual rates data are even more useful at the metro level. NIC MAP Vision is continuing to work towards reporting more markets.

The Actual Rates Data Initiative is an effort to expand senior housing data and we are looking for operators who have five or more properties to participate. We have expertise in extracting data from industry leading software systems, such as Yardi, PointClickCare, Alis, MatrixCare, Glennis Solutions, and Eldermark and can facilitate the process for you.

Operators contributing data to the NIC MAP Vision Seniors Housing Actual Rates Report receive a complimentary report which allows them to compare their own data against national, and metropolitan market benchmarks.

In addition to receiving a complimentary report, your organization benefits through: