Insights in Seniors Housing & Care

A recent NIC Notes blog titled “Market Fundamentals Amid Challenging Time for Skilled Nursing” published by NIC Analytics, evaluated supply and demand dynamics for freestanding skilled nursing properties within the 31 NIC MAP Primary Markets (Primary Markets) aggregate since 2017, and examined property-level occupancy distribution to get a better understanding of how widespread the effects of the pandemic have been.

This analysis digs further and reviews how select individual skilled nursing markets are faring after two years of the pandemic.

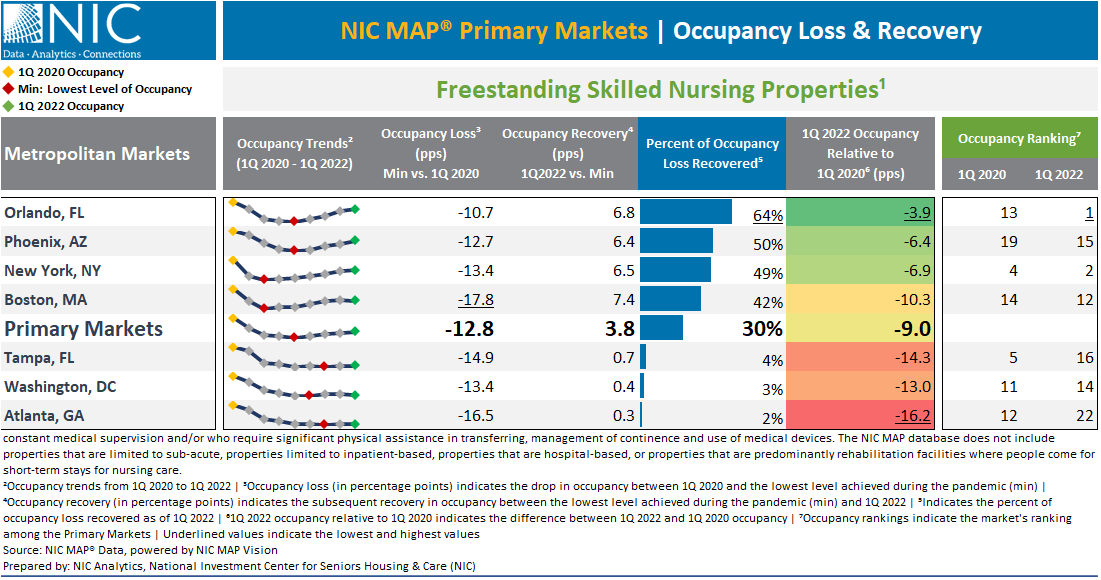

Occupancy Loss and Recovery Varied by Market. During the height of the pandemic, the occupancy loss for freestanding skilled nursing properties across all the Primary Markets was mainly a function of a demand contraction. In fact, inventory across most of the Primary Markets remained somewhat stable over the period from 1Q 2020 to 1Q 2021.

Drilling down into metropolitan markets, Boston’s occupancy fell 17.8 percentage points (pps) from 88.7% in first quarter 2020 to 70.9% in third quarter 2020. As a result, occupied units in Boston fell by nearly 21% in the span of two quarters. This was the largest demand contraction and occupancy loss a market experienced in the first two quarters of the pandemic. New York also experienced a large drop in occupancy. In the early months of the pandemic, New York’s occupancy rate fell 13.4pps from 92.0% in the first quarter of 2020 to 78.6% in the third quarter of 2020.

Notably, all the Primary Markets experienced double-digit occupancy declines, except Dallas (negative 9.6pps) and Kansas City (negative 7.7pps). Additionally, none of the skilled nursing Primary Markets experienced significant inventory growth during the height of the pandemic. Therefore, the skilled nursing occupancy declines were mainly a function of demand contraction whereas the occupancy loss for the private pay senior housing sector was a function of both an increase in supply and a decrease in demand.

On the other hand, the occupancy recovery paths and timelines are also proving to be uneven across markets with select Primary Markets improving more rapidly than others. For example, Orlando is a market that experienced a relatively smaller drop in occupancy during the first year of the pandemic of 10.7pps, from 89.7% in the first quarter of 2020 to 79.0% in the first quarter of 2021. However, Orlando’s occupancy increased by 6.8pps during the second year of the pandemic and stood at 85.9% in the first quarter of 2022. This helped the market recover 64% of the occupancy loss in percentage points and pushed its occupancy ranking from thirteenth to first among the Primary Markets.

The exhibit below shows that occupancy across several markets is recovering relatively fast. These markets include Orlando, Phoenix, New York, and Boston. Notably, 17 of the 31 Primary Markets have recovered at least 30% of the occupancy loss in percentage points, although occupancy across some of these markets is still far below pre-pandemic levels.

While the occupancy improvements across most Primary Markets depict a very welcome positive trend and indicate light on the horizon, the uncertainty bands remain wide in terms of when occupancy rates for skilled nursing properties will return to pre-pandemic levels. A key question is whether obtaining a sustainable level of occupancy and revenue growth will be sufficient to grow NOI and recoup some of the losses associated with the severe downturn in occupancy rates, higher expenses associated with agency staffing, PPE and other costs, Medicare funding cuts, and underfunding of Medicaid reimbursement in many states. Other headwinds for NOI growth include staffing shortages that are effectively restricting admissions of residents into some skilled nursing properties, and broader inflationary effects associated with the pandemic.

For example, a few markets experienced prolonged occupancy pullbacks and the recovery has thus far been elusive. This is the case of Tampa where 1Q 2022 occupancy remained 14.3pps below pre-pandemic 1Q 2020 levels and shifted the market’s ranking among the Primary Markets from fifth to sixteenth. Similarly, Washington and Atlanta are markets that experienced prolonged occupancy declines and remained far below pre-pandemic levels.

We cannot yet know how pandemic-derived challenges will unfold in future months, or when they will be fully behind us, but the skilled nursing industry has weathered this extremely difficult period and begun the path to recovery.

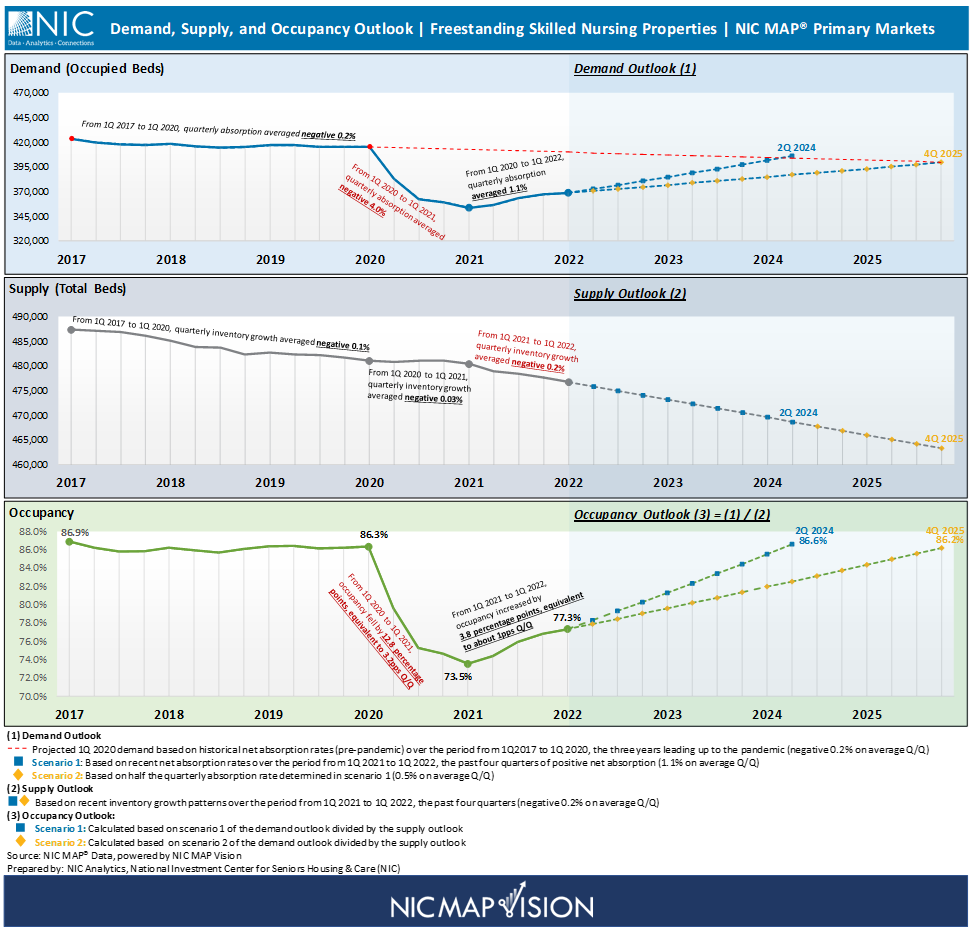

Skilled Nursing Occupancy Outlook - NIC MAP 31 Primary Markets aggregate

Historical data highlights of exhibit 2 below, along with expert analysis and commentary, are provided in the recently published blog by NIC Analytics. This analysis focuses more on future outlook and provides outlook scenarios of demand and supply to gauge when skilled nursing occupancy for the Primary Markets aggregate will likely return to pre-pandemic 1Q 2020 levels. The occupancy outlook scenarios are based solely on recent patterns and growth measures of supply and demand.

Demand Outlook

As background, demand for freestanding skilled nursing properties was contracting even prior to the pandemic. Based on historical data since 2017, quarterly net absorption rates averaged negative 0.2%, over the period from 1Q 2017 to 1Q 2020, the three years preceding the pandemic. Given the negative demand growth witnessed prior to the pandemic, demand would have likely continued to decline even if the pandemic never happened as depicted by the red dotted line on exhibit 2 below, defined as projected 1Q 2020 demand based on historical net absorption rates (pre-pandemic) over the period from 1Q 2017 to 1Q 2020 (negative 0.2% on average quarter-to-quarter).

Scenario 1 – Over the period from 1Q 2021 to 1Q 2022, the past four quarters of positive net absorption, the quarterly growth in occupied units for the 31 Primary Markets averaged 1.1% (quarter-to-quarter). Assuming on this quarterly demand growth measure, occupied units would likely recover and return to projected 1Q 2020 levels by midyear 2024 (2Q 2024).

Scenario 2 – During the past four quarters (1Q 2020 to 1Q 2022), demand for freestanding skilled nursing properties has been increasing at an unprecedented pace. Given that the sector still has challenges due to the ongoing pandemic, this second scenario provides a more “conservative” approach of when occupied units could recover (half the quarterly absorption rate determined in scenario 1, equivalent to 0.5% on average quarter-to-quarter). Based on this more “conservative” scenario, occupied units would likely recover and return to projected 1Q 2020 levels by 4Q 2023.

Supply Outlook

During the second year of the pandemic (1Q 2021 to 1Q 2022), the skilled nursing inventory contraction accelerated once again, averaging negative 0.2% quarter-to quarter, twice the rate recorded prior to the pandemic (negative 0.1% quarter-to-quarter over the three years leading up to the pandemic, from 1Q 2017 to 1Q 2020), and nearly seven times the rate recorded during the first year of the pandemic (negative 0.03% quarter-to-quarter over the period from 1Q 2020 to 1Q 2021).

Taking into account the very low occupancy rates and the pandemic-derived challenges noted above the skilled nursing sector continues to face, inventory would likely continue to decline relatively fast. The supply outlook trend depicted on exhibit 2 below is based on recent inventory growth patterns over the period from 1Q 2021 to 1Q 2022 (negative 0.2% on average quarter-to-quarter).

Occupancy Outlook

We cannot yet know how pandemic-derived challenges will unfold in future months, or when they will be fully behind us, but the skilled nursing industry has weathered this extremely difficult period and begun the path to recovery.

Upon calculation of occupancy based on occupied units (demand) and total units (supply) from the scenarios above, occupancy could return to its pre-pandemic 1Q 2020 levels between midyear 2024 and end of the year 2025.

This analysis examined approximately 4,000 freestanding skilled nursing properties within the Primary Markets. Note that combined properties offering at least two types of service and life plan communities (LPCs)/continuing care retirement communities (CCRCs) were excluded from this analysis.

---

To learn more about NIC MAP data, powered by NIC MAP Vision, an affiliate of NIC, and accessing the data featured in this article, schedule a meeting with a product expert today.

Beth Burnham Mace is a special advisor to the National Investment Center for Seniors Housing & Care (NIC) focused exclusively on monitoring and reporting changes in capital markets impacting senior housing and care investments and operations. Mace served as Chief Economist and Director of Research and Analytics during her nine-year tenure on NIC’s leadership team. Before joining the NIC staff in 2014, Mace served on the NIC Board of Directors and chaired its Research Committee. She was also a director at AEW Capital Management and worked in the AEW Research Group for 17 years. Prior to joining AEW, Mace spent 10 years at Standard & Poor’s DRI/McGraw-Hill as director of its Regional Information Service. She also worked as a regional economist at Crocker Bank, and for the National Commission on Air Quality, the Brookings Institution, and Boston Edison. Mace is currently a member of the Institutional Real Estate Americas Editorial Advisory Board. In 2020, Mace was inducted into the McKnight’s Women of Distinction Hall of Honor. In 2014, she was appointed a fellow at the Homer Hoyt Institute and was awarded the title of a “Woman of Influence” in commercial real estate by Real Estate Forum Magazine and Globe Street. Mace earned an undergraduate degree from Mount Holyoke College and a master’s degree from the University of California. She also earned a Certified Business Economist™ designation from the National Association of Business Economists.

Omar Zahraoui, Principal at the National Investment Center for Seniors Housing & Care (NIC), is a seniors housing research professional with expertise in providing quantitative analysis and insights on seniors housing & care market data; building new products and reporting capabilities, including dashboards and proformas for clients and internal stakeholders; and implementing new processes and data solutions. Prior to his current role, Omar worked as a data analyst, at Calpine Corporation, supporting the development of new-business strategy initiatives, analyzing sales and financial data, and developing statistical modeling of consumers’ behaviors to drive business performance. Omar holds a Bachelor’s degree in Business Administration with concentrations in Finance and Management, a Master in Corporate Finance from IAE Lyon School of Management at Jean Moulin Lyon III University in France, and a Master of Science in Management Information Systems and Data Analytics from Pace University.

Connect with Beth Mace and Omar Zahraoui