Insights in Seniors Housing & Care

By: Lana Peck | January 09, 2019

CCRC | Economic Trends | Market Trends | Senior Housing | Skilled Nursing | Workforce

Expanding on a recent NIC blog post that detailed care segment performance in the NIC MAP® 31 Primary Markets since the most recent Q42014 market cycle peak, and another blog post that went a step further and examined segment market fundamentals within Continuing Care Retirement Communities (CCRCs, also referred to as life plan communities) compared with those in non-CCRC freestanding or combined communities, the following narrative describes 3Q2018 CCRC occupancy aggregated from the NIC MAP Primary and Secondary Markets—99 of the nation’s largest core-based statistical areas (CBSAs), broken out across eight regions.

This analysis is useful for understanding the regional occupancy performance of independent living, assisted living, memory care and nursing care segments. The occupancy rate used was the “all occupancy” rate which includes units still in lease-up as well as those occupied.

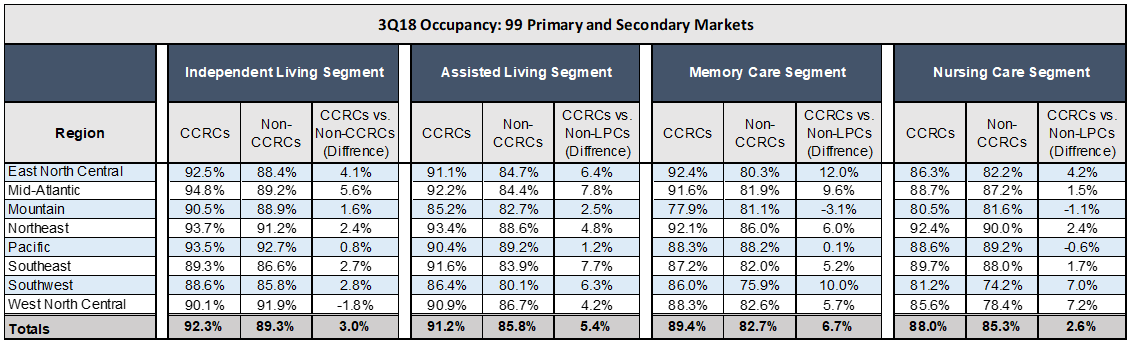

Regional CCRC Care Segment Occupancy

Overall, the Northeast and Mid-Atlantic regions had the strongest performance in terms of CCRC occupancy across care segments, whereas the Mountain and Southwest regions performed relatively weaker.

CCRC Segments vs. Non-CCRC Segments

Across all regions, 3Q18 CCRC occupancy in the 99 Primary and Secondary metropolitan markets was 90.8%; five percentage points higher than non-CCRCs (85.8%). Generally speaking, this difference is perhaps due in part to the CCRC product profile, which tends to attract planners who wish to make one move to a continuum of care, or perhaps because new CCRC residents are generally healthier than residents in other types of seniors housing, resulting in lower resident turnover in CCRCs. Another potential reason for the difference is perhaps due to the inventory mix in the CCRC analysis aggregation (both entrance fee and rental payment options, combined). Note that 98.8% of non-CCRC segments were rental, whereas CCRC segments were comprised of 63.3% entrance fee and 36.7% rental payment models.

Interestingly, across care segments, occupancy at CCRCs was also generally higher than non-CCRCs. By care segment, the greatest differences in occupancy rates for CCRCs compared with non-CCRCs were reported for the memory care segment (6.7 percentage points), followed by the assisted living segment (5.4 percentage points), and the narrowest for the nursing care segment (2.6 percentage points).

Non-CCRCs had higher occupancy than CCRCs in the following care segments by region: independent living in the West North Central region (a difference of 1.8 percentage points), memory care in the Mountain region (a difference of 3.1 percentage points), and nursing care in the Mountain and Pacific regions (differences of 1.1 and 0.6 percentage points, respectively).

Further analysis is needed to more fully explain regional differences in CCRC occupancy performance in comparison to non-CCRC segments. Contributing factors that could be explored include economic drivers such as industry mix, cost of doing business and living costs, employment growth, the health of the residential housing market in terms of home sales prices and velocity. Other considerations include income levels, inflation-adjusted purchasing power, prospective resident educational profiles, product acceptance and familiarity as well as penetration rates, longevity of the CCRC product in the area, and cultural differences.

The second installment of this two-part blog post will compare the regional occupancy performance of entrance fee and rental CCRCs.

Lana Peck, former senior principal at the National Investment Center for Seniors Housing & Care (NIC), is a seniors housing market intelligence research professional with expertise in voice of customer analytics, product pricing and development, market segmentation, and market feasibility studies including demand analyses of greenfield developments, expansions, repositionings, and acquisition projects across the nation. Prior to joining NIC, Lana worked as director of research responsible for designing and executing seniors housing research for both for-profit and nonprofit communities, systems and national senior living trade organizations. Lana’s prior experience also includes more than a decade as senior market research analyst with one of the largest senior living owner-operators in the country. She holds a Master of Science, Business Management, a Master of Family and Consumer Sciences, Gerontology, and a professional certificate in Real Estate Finance and Development from Massachusetts Institute of Technology (MIT).

Connect with Lana Peck