It’s no secret that the U.S. population of seniors living with dementia is expected to grow in the coming years and thus the demand for memory care (MC) services is expected to increase as well. As a result of anticipated demand, there has been notable growth in memory care units, especially between 2011 and 2016. This has occurred in freestanding memory care properties as well as in properties that offer memory care as part of a continuum of service offerings. This blog post explores these trends and looks at how well demand has held up and its resulting effects on occupancy. Read further for a deeper dive into memory care in the Primary Markets.

What Do We Mean by Freestanding Memory Care?

Freestanding memory care communities offer memory care as the only level of care, whether these properties have a single building, or several. Because many freestanding memory care properties have smaller unit counts than other seniors housing properties, NIC tracks those that have 16 or more units, rather than the 25 or more units and/or nursing care beds that we require at other types of properties.

The community type data cut was first introduced to the NIC MAP® portal in 2016, partially in response to a growing request from our client base to be able to separate out properties that had a majority of memory care units or properties that were freestanding memory care. As of 1Q2019, 89% of the memory care communities that were open for business in the Primary Markets were freestanding, meaning only 11% were combined properties, and none were continuing care retirement communities (CCRCS). CCRCs are distinct from all other community types using this categorization and require both independent living and nursing care to exist on the same property. Additionally, 97% of all the open MC communities in the Primary Markets were operated by for-profit operators in 1Q2019.

Freestanding memory care communities are relatively young among the community types that NIC tracks, with a median age of having been open for 16 years versus 19.5 years for independent living communities, 20 years for assisted living communities, 40 years for nursing care communities, and 35 years for CCRCs for the Primary Markets as of 1Q19. This reflects freestanding memory care being the newest product type offered among the group.

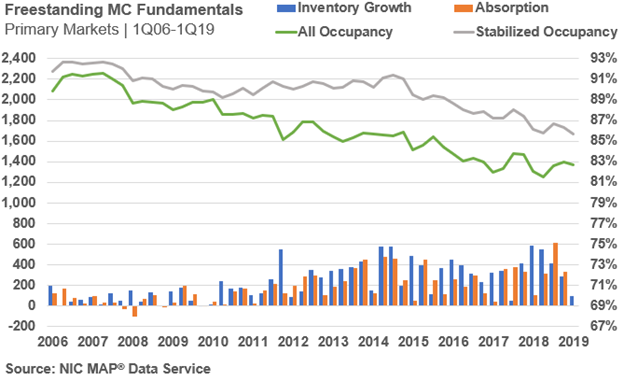

Has occupancy hit the bottom for freestanding memory care in the Primary Markets?

The chart above shows market fundamentals for freestanding memory care communities in the Primary Markets since 2006 when NIC began reporting the data. The broad trend since then has been falling occupancy rates as inventory growth outpaced demand (as measured by net absorption). Occupancy reached a recent low of 81.5% in the second quarter of 2018 as historical inventory growth dwarfed net demand by more than one third (11,743 units of inventory growth versus 8,438 units of net demand from Q1 2006 to Q2 2018). Since then, freestanding memory care occupancy has increased by 120 basis points to 82.7% in Q1 2019. Stabilized occupancy stood at 85.7% in 1Q2019, 300 basis points higher than total occupancy, reflecting many units that have been opened, but not yet leased.

The occupancy improvement reflects a strong year for freestanding memory care communities with 1,360 net units absorbed in 2018. The strongest recorded quarterly absorption for these communities was 611 units in 3Q2018. The strongest recorded quarterly inventory growth occurred in 1Q2018 with net 588 units coming online.

By Segment, Annual Inventory Growth meets Annual Absorption in 1Q2019.

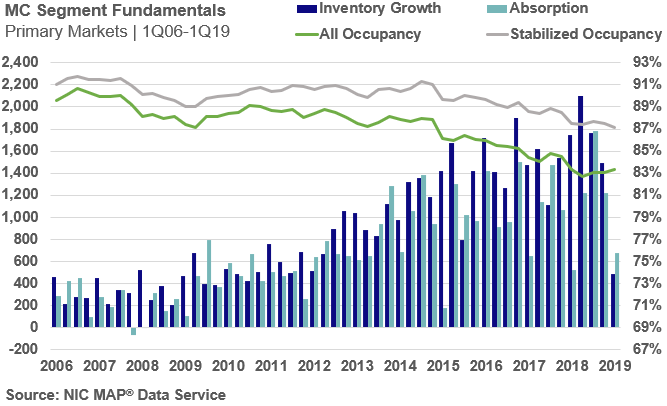

Freestanding memory care communities only account for 29.3% of the open memory care units in the Primary Markets. Looking at all memory care as a segment (i.e.: all open memory care units regardless of the property in which they are located), total open inventory in 1Q2019 equaled 87,025 units versus 25,472 units in freestanding memory care.

The same broad trends of declining occupancy rates as inventory growth outpaced demand occurred for memory care as a segment. The occupancy rate in the first quarter was 83.3% compared with 82.7% for stand-alone memory care units.

It’s notable that net demand in the first quarter was stronger than in freestanding memory care (where net absorption was negative 1 unit), with 674 units absorbed in the memory care segment in the Primary Markets. That figure is down 541 units from 1,215 in the fourth quarter of 2018 but is up from 525 a year earlier in 1Q2018. Interesting to note is the recorded high of 1,778 units for memory care absorption for the Primary Markets in 3Q2018.

Inventory growth of memory care units for the Primary Markets for 1Q2019 totaled 489 units, the fewest since 3Q2010, and 1,001 units less than 4Q2018’s inventory growth of 1,490 units. The recorded high for memory care inventory growth for the Primary Markets was 2,097 units in 2Q2018.

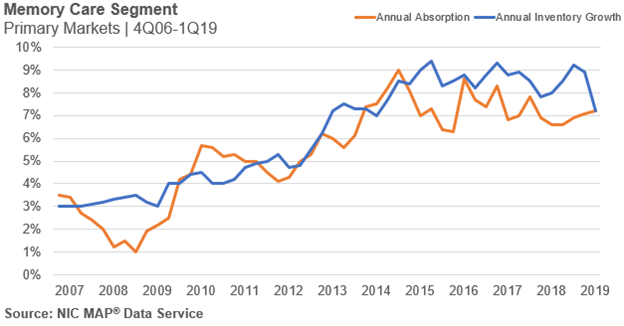

The chart below shows annual absorption (year-over-year percent change in occupied units) and annual inventory growth. Both demand and supply show upward trends in the years since NIC has been reporting the data. The annual absorption and annual inventory growth for memory care for 1Q2019 were both 7.2%. This made 1Q2019 the first quarter where the annual inventory growth rate didn’t outpace the annual absorption rate since 3Q2014.

Opportunity exists for seniors housing.

Data through the first quarter of 2019 suggests that the bottom may have been reached for occupancy for both stand alone and continuum memory care units. Nevertheless, with occupancy still in the low 80% range, the sector faces challenges as operators and investors seek to meet their business plan requirements and pro formas. Although the first quarter of 2019 had some softer absorption and inventory growth, record high inventory growth and absorption occurred for both freestanding memory care communities and memory care as a segment in 2018. The market will need some time to better establish an equilibrium position. Because of current predictions of rising dementia rates, and the special considerations associated with serving this population, operators who offer memory care should not only anticipate potential changes in demand when planning their offerings but also how to recruit and keep excellent employees who understand the needs of this population. While some investors prefer to partner with best-in-class operators with strong experience in stand-alone memory care with focused memory care offerings, others prefer operators with properties that offer multiple care levels to serve a wider range of needs (often AL and MC).