“Executive Survey Insights results suggest that the seniors housing and care market fundamentals may have reached a turning point at the end of March 2021. According to survey respondents, leads volume continues to grow and the shares of organizations reporting accelerations in move-ins continues to trend positively. These leading indicators have been translating into higher occupancy rates since the Wave 25 survey, conducted in the latter half of March.”

–Lana Peck, Senior Principal, NIC

NIC’s Executive Survey of operators in seniors housing and skilled nursing is designed to deliver transparency into market fundamentals in the seniors housing and care space as market conditions continue to change. This Wave 28 survey includes responses collected May 3 to May 16, 2021 from owners and executives of 64 small, medium, and large seniors housing and skilled nursing operators from across the nation, representing hundreds of buildings and thousands of units across respondents’ portfolios of properties.

Detailed reports for each “wave” of the survey and a PDF of the report charts can be found on the NIC COVID-19 Resource Center webpage under Executive Survey Insights.

Wave 28 Summary of Insights and Findings

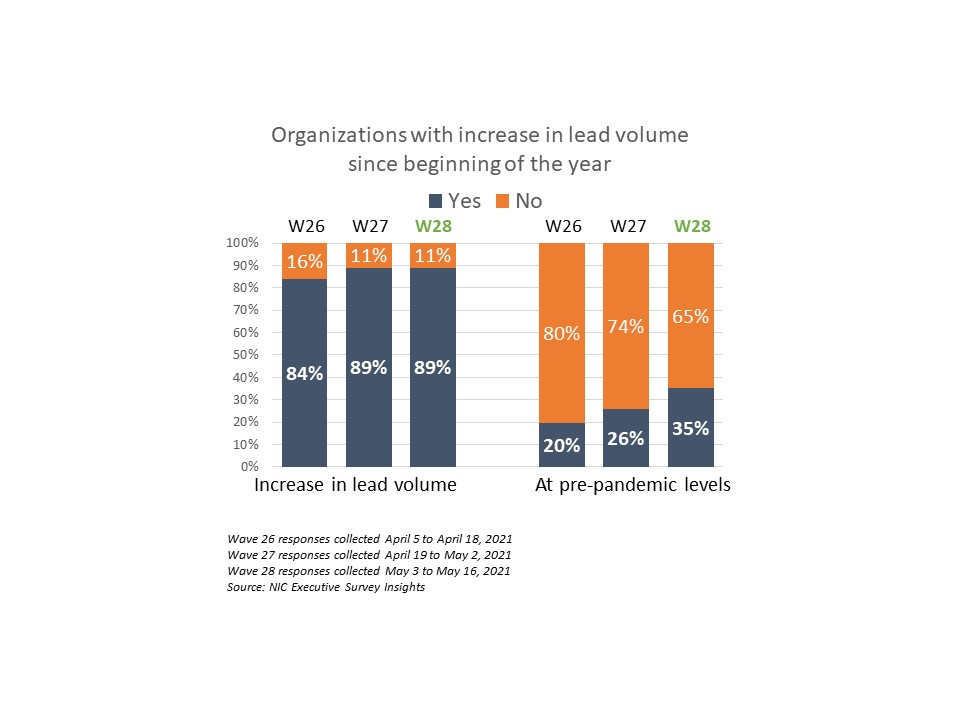

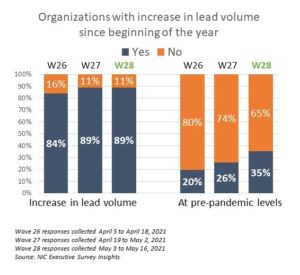

- Since early April, respondents were asked if their organizations had seen an increase in resident lead volume since the beginning of the year—and if they had—if lead volume is above pre-pandemic levels, As shown in the chart below, about nine out of ten organizations reported an increase in lead volume (89%). Additionally, one-third of organizations report lead volume currently above pre-pandemic levels (35%) compared to 20% in Wave 26 conducted just one month ago. Regardless of reports of notable improvement in lead volume, nearly two-thirds of survey respondents expect their organizations’ occupancy rates to recover to pre-pandemic levels sometime in 2022. This sentiment has remained consistent since first reported in late February (Wave 23).

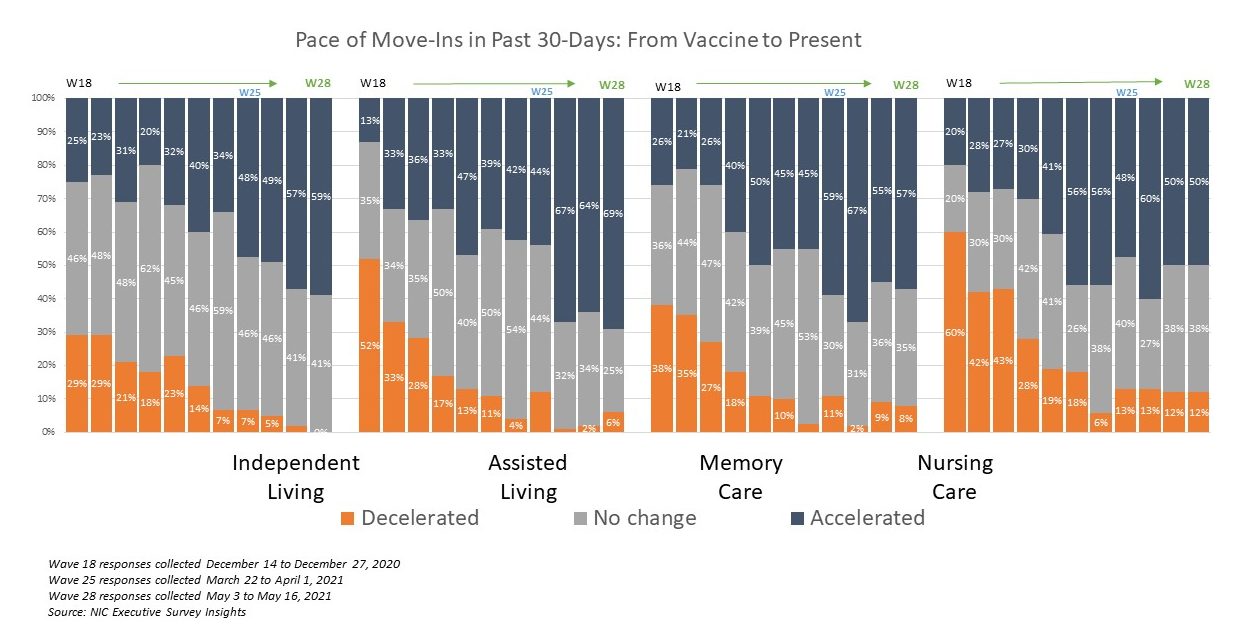

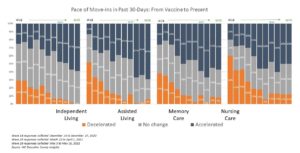

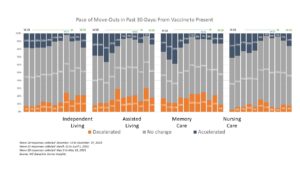

- The strongest reports of move-ins increasing began generally in and around the Wave 25 survey conducted at the end of March (however, sooner for the nursing care segment). In other words, acceleration in the pace of move-ins became notable near the end of the first quarter of 2021.

- Interestingly, increased resident demand has been cited by nine out of ten respondents as a reason for acceleration in move-ins since the Wave 25 survey. And, since then, the average rates of resident and staff vaccinations have leveled off at around 90% of residents and 65% of staff.

- The chart below shows the shares of organizations reporting acceleration, deceleration, or no change in the pace of move-ins by care segment—across their portfolios of properties—since the COVID-19 vaccine began to be distributed in the latter half of December (survey Wave 18) to the present. (For a key to the specific dates of these survey waves, please click here.)

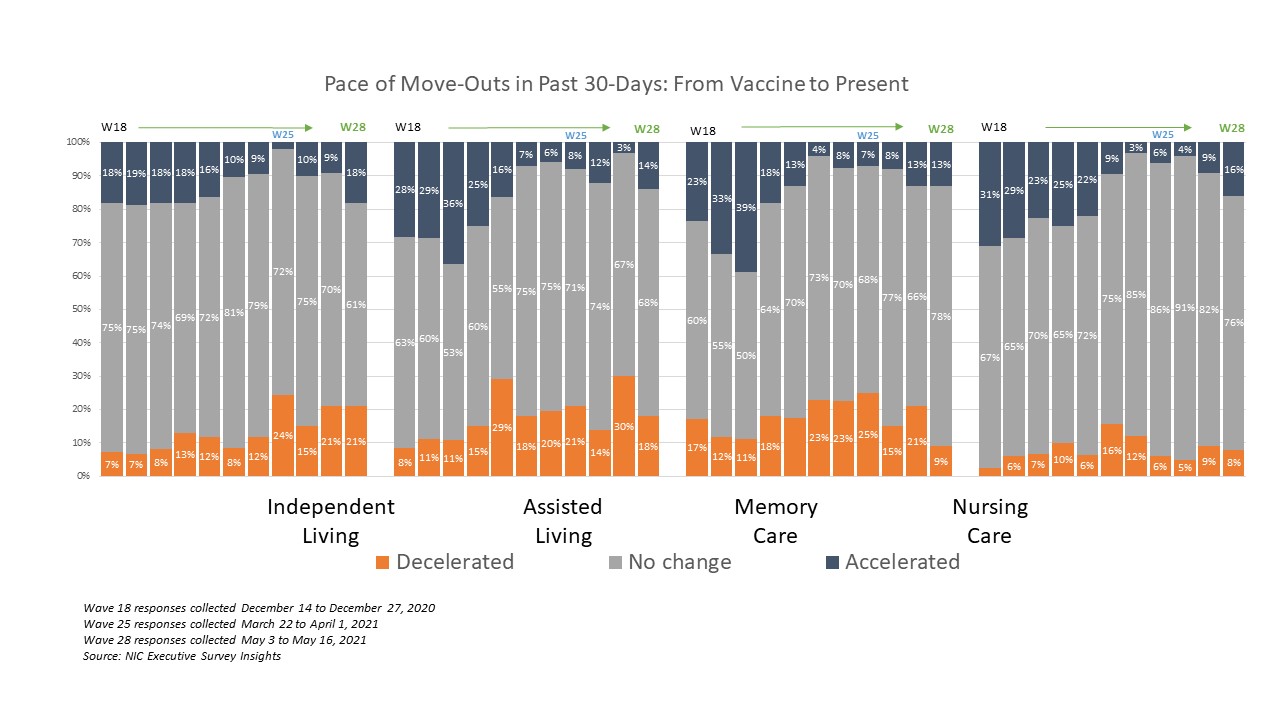

- Regarding trends in the pace of move-outs, the most recent and slight increase was mainly attributed to transfers to higher levels of care, followed by normal attrition according to survey respondents.

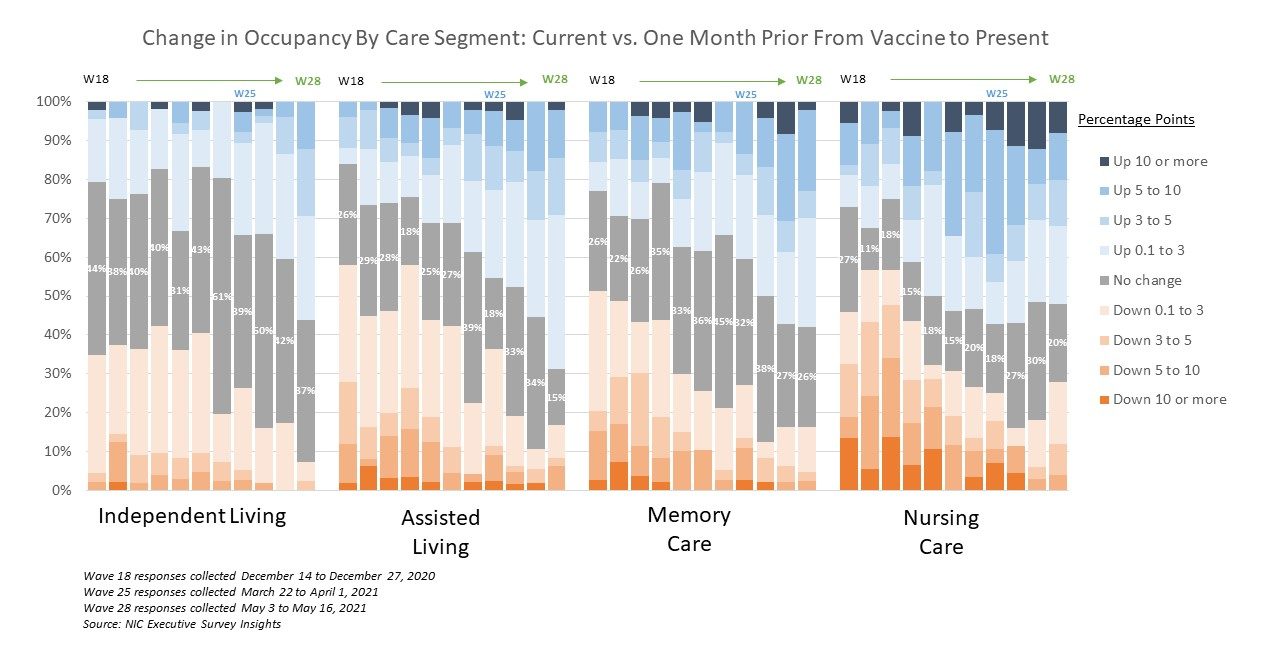

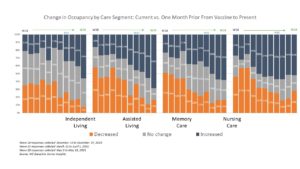

- The chart below depicts a compelling trend in the shares of organizations reporting higher occupancy since the Wave 25 survey conducted at the end of March. Roughly 50% to 70% reported upward changes in occupancy in the Wave 28 survey. (For a key to the specific dates of these survey waves, please click here.)

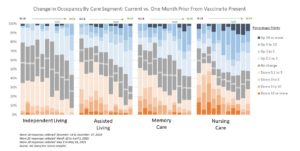

- The degrees of occupancy change variation are shown in the chart below starting with survey Wave 18. Stronger improvement in the change in occupancy rates in recent waves of the survey support the inference that signs of recovery now appear more solid trends as supported by the length and depth of the blue stacked bar segments.

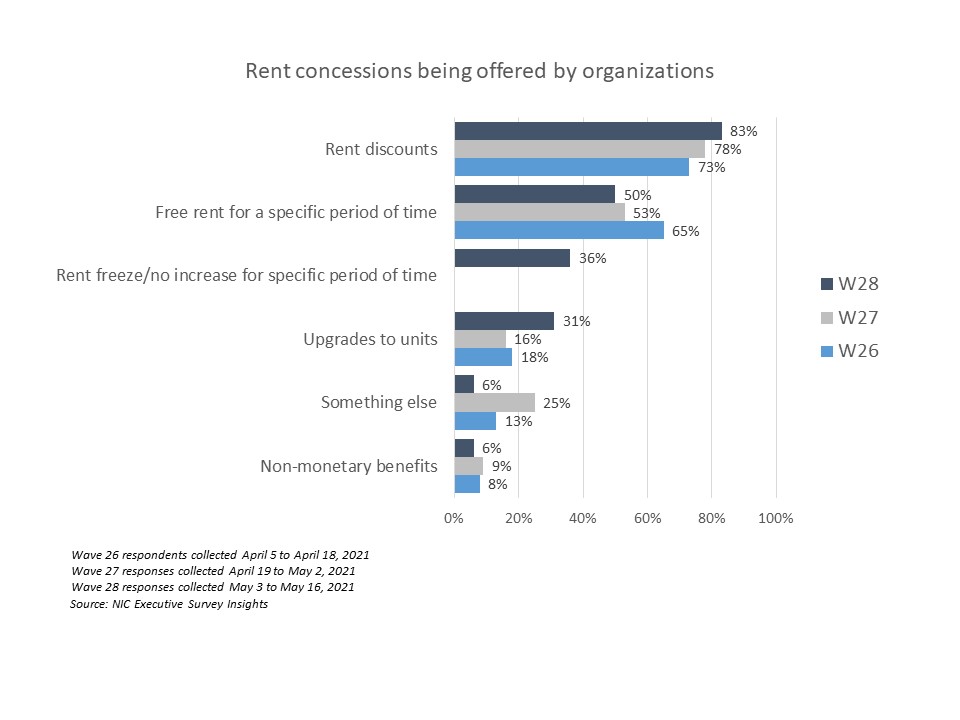

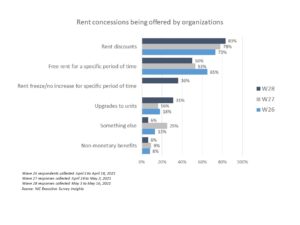

- Three out of five respondent organizations were offering rent concessions to attract new residents. As shown in the chart, four out of five of them were discounting monthly rents (83% in Wave 28 vs. 73% in Wave 26). One-half of organizations in Wave 28 (50%) were offering free rent for a specified period, down from two-thirds in Wave 26 (65%). Rent freezes, which were written in by survey respondents as “something else” were quantified in Wave 28 with about one-third (36%) capping rents for new residents for a specific period (e.g., two-years). Other tactics include community fee discounts, waiving second person fees, and giving moving allowances.

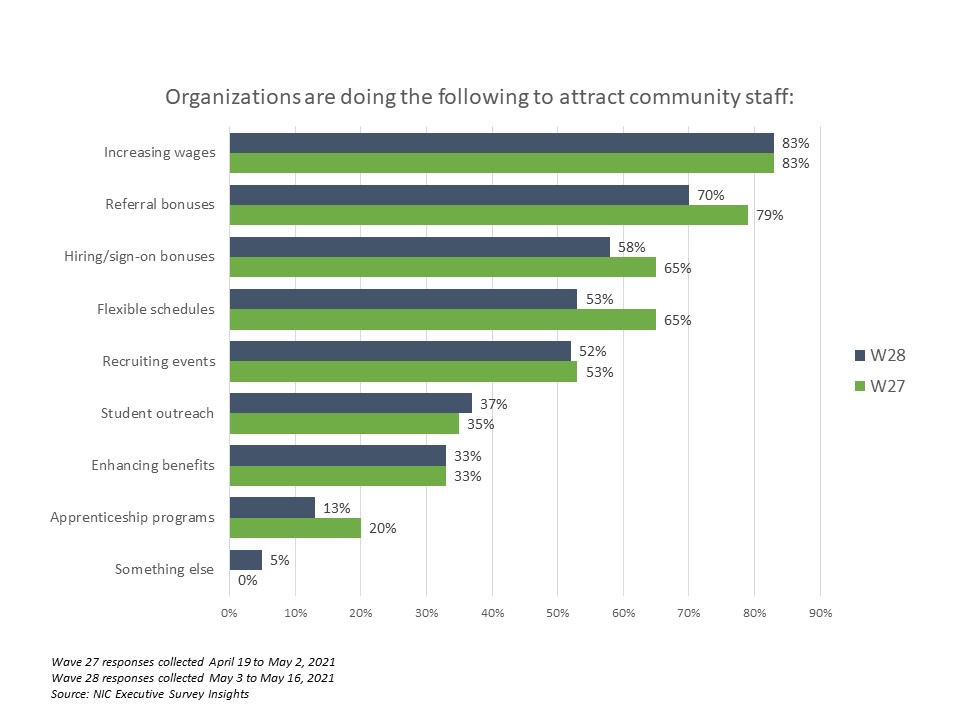

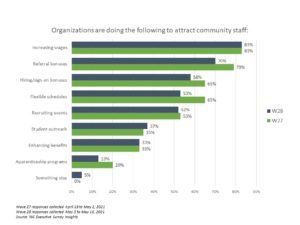

- In the Wave 28 survey, the share of organizations experiencing staffing shortages in their properties has leveled off at a very high 90%. Before the pandemic, operators were challenged with labor shortages due to widespread and generally low unemployment rates. During the pandemic, the problem was exacerbated by employees leaving the workforce.

- To attract community staff, most respondent organizations are increasing wages, offering referral bonuses, and more than half are offering hiring/sign-on bonuses. Staff wages and benefits are typically the most significant operating expenses for seniors housing and care providers. NOI has been squeezed by the efforts to replace workers who left the labor force during the pandemic, coupled with months of receding occupancy rates that had fallen to historic lows in the first quarter of 2021.

Wave 28 Survey Demographics

- Responses were collected between May 3 to16, 2021 from owners and executives of 64 seniors housing and skilled nursing operators from across the nation. Owner/operators with 1 to 10 properties comprise 61% of the sample. Operators with 11 to 25 and 26 properties or more make up 39% of the sample (25% and 14%, respectively).

- More than one-half of respondents are exclusively for-profit providers (61%), roughly one-quarter (27%) are nonprofit providers, and 11% operate both for-profit and nonprofit seniors housing and care organizations.

- Many respondents in the sample report operating combinations of property types. Across their entire portfolios of properties, 81% of the organizations operate seniors housing properties (IL, AL, MC), 21% operate nursing care properties, and 34% operate CCRCs (aka Life Plan Communities).

Owners and C-suite executives of seniors housing and care properties, please help us tell an accurate story about our industry’s performance. Now, more than ever, we need your response so that we can track firsthand the inflection point on occupancy. This will be a turning point and we want all of our industry stakeholders to know when this important moment occurs.

The current survey is available and takes 5 minutes to complete. If you are an owner or C-suite executive of seniors housing and care and have not received an email invitation to take the survey, please click this link, which will take you there.

NIC wishes to thank survey respondents for their valuable input and continuing support for this effort to bring clarity and create a comprehensive and honest narrative in the seniors housing and care space at a time when trends are continuing to change in our sector

About Lana Peck

Lana Peck, former senior principal at the National Investment Center for Seniors Housing & Care (NIC), is a seniors housing market intelligence research professional with expertise in voice of customer analytics, product pricing and development, market segmentation, and market feasibility studies including demand analyses of greenfield developments, expansions, repositionings, and acquisition projects across the nation. Prior to joining NIC, Lana worked as director of research responsible for designing and executing seniors housing research for both for-profit and nonprofit communities, systems and national senior living trade organizations. Lana’s prior experience also includes more than a decade as senior market research analyst with one of the largest senior living owner-operators in the country. She holds a Master of Science, Business Management, a Master of Family and Consumer Sciences, Gerontology, and a professional certificate in Real Estate Finance and Development from Massachusetts Institute of Technology (MIT).

Connect with Lana Peck

Read More by Lana Peck