NIC’s Executive Survey of operators in seniors housing and skilled nursing is designed to deliver transparency into market fundamentals in the seniors housing and care space at a time when market conditions continue to change—providing both capital providers and capital seekers with data as to how COVID-19 is impacting the sector.

This Wave 12 survey sample includes responses collected September 15- 27, 2020 from owners and executives of 67 seniors housing and skilled nursing operators from across the nation. Detailed reports for each “wave” of the survey can be found on the NIC COVID-19 Resource Center webpage under Executive Survey Insights.

Wave 12 Summary of Insights and Findings

Several themes emerged from the results of Wave 12: battling the pandemic is putting strain on operating costs; resident or family member concerns cited by survey respondents as a reason for declines in the pace of move-ins remain high; there has been significant improvement in time receiving COVID-19 test results; resident demand is increasing; and more organizations are using agency or temp staff to fill staffing vacancies. In Wave 12, more than half of respondents (57%) were tapping agency or temp staff to mitigate staffing shortages—up from 36% in Wave 3—adding to increasing operating costs since the pandemic began. Further, while more organizations continue to ease move-in restrictions, the share of survey respondents offering rent concessions to attract new residents in Wave 12 has grown since Wave 10 from approximately one-third to one-half.

- Roughly two-thirds (61%) of organizations were easing move-in restrictions in some or all of their locations in Wave 12, up from roughly half in the prior two waves of the survey. Fewer than one in ten organizations in the past two waves were increasing move-in restrictions, presumably due to temporary local and/or state government mandates for move-in moratoriums when a staff or resident in a community tests positive for COVID-19. Organizations citing a moratorium on move-ins as reason for deceleration in the pace of move-ins is at the lowest level in the time series (15%).

- In Wave 12, more organizations with memory care units reported an acceleration in the pace of move-ins than in any other wave of the survey (51%). This may be simply due to increased demand, and/or it may be due to resident-attracting discounts as half of operators with memory care units (freestanding and/or combined with other care segments) reported offering rent concessions in Wave 12.

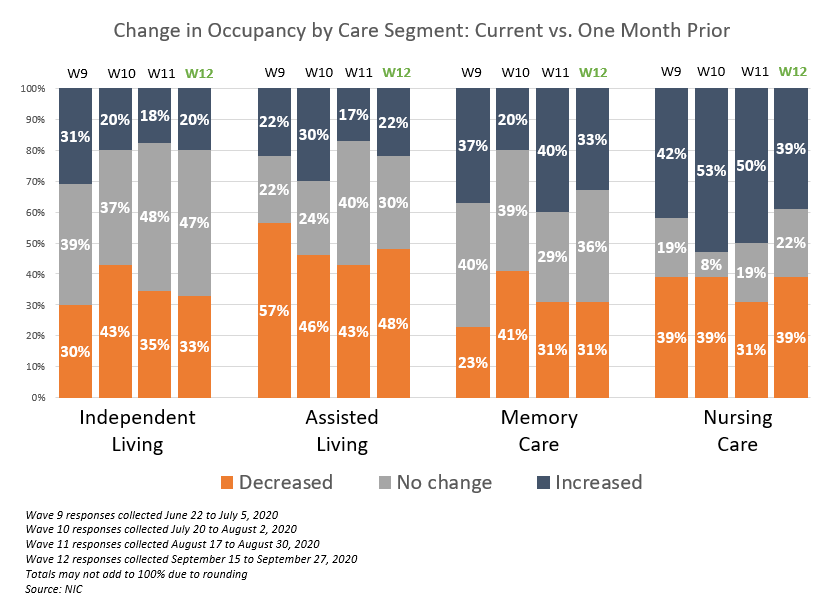

- Although more organizations with memory care units reported an acceleration in move-ins in Wave 12, roughly one-third report an increase in occupancy rates from one month prior, down from 40% in Wave 11. The shares of organizations with independent living units and nursing care beds that report no change or increasing occupancy remain similar to recent waves of the survey. However, roughly half of organizations with assisted living units reported month-over-month downward changes in occupancy rates in Wave 12.

- Organizations with nursing care beds reporting accelerations in the pace of move-ins retreated to Wave 8-levels surveyed in late May to early June. Respondents citing hospital placement of residents as a reason for an acceleration in move-ins has waned somewhat since the initial surge of hospitals resuming elective surgeries.

- Significantly, the availability of PPE and COVID-19 testing kits improved in recent waves of the survey. In Wave 12, about three in five respondents (59%) reportedly had little difficulty obtaining PPE, up from about one in four in Wave 10 (27%). Additionally, roughly half in Waves 11 and 12 note considerable improvement in obtaining COVID-19 testing kits, up from about one-quarter in Wave 10.

- The time frame for receiving COVID-19 test results has also improved significantly over prior waves of the survey. In Wave 12, 43% of organizations indicated their test results were being returned within 2 days. Nevertheless, just over half (57%) note that it still takes three or more days to receive test results, however, this is down from 87% in Wave 10.

Wave 12 Survey Demographics

- Responses were collected September 15-September 27, 2020 from owners and executives of 67 seniors housing and skilled nursing operators from across the nation. Roughly half of respondents are exclusively for-profit providers (52%), about one-third (36%) are exclusively nonprofit providers, and 12% operate both for-profit and nonprofit seniors housing and care organizations.

- Owner/operators with 1 to 10 properties comprise 61% of the sample. Operators with 11 to 25 properties make up 22% of the sample, while operators with 26 properties or more make up 17% of the sample.

- Many respondents in the sample report operating combinations of property types. Across their entire portfolios of properties, 81% of the organizations operate seniors housing properties (IL, AL, MC), 31% operate nursing care properties, and 34% operate CCRCs (aka Life Plan Communities).

Key Survey Results

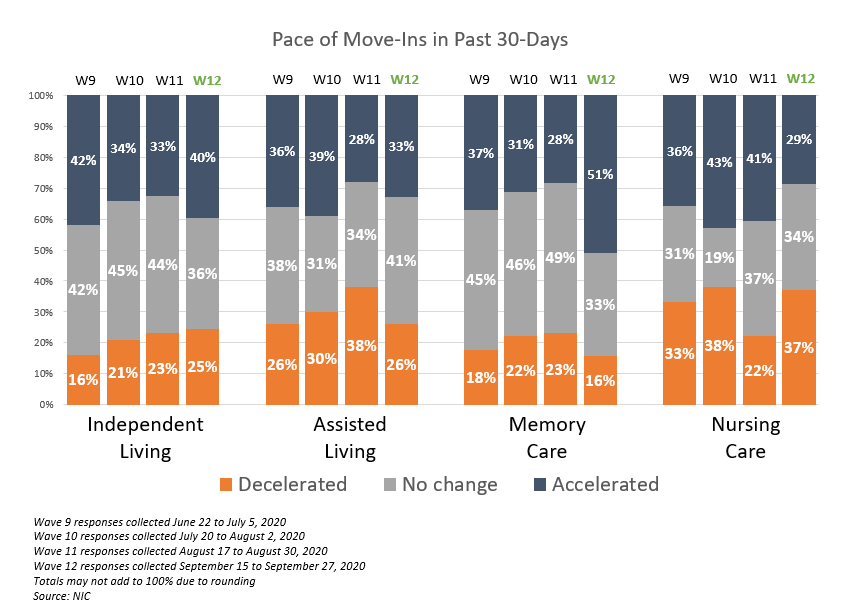

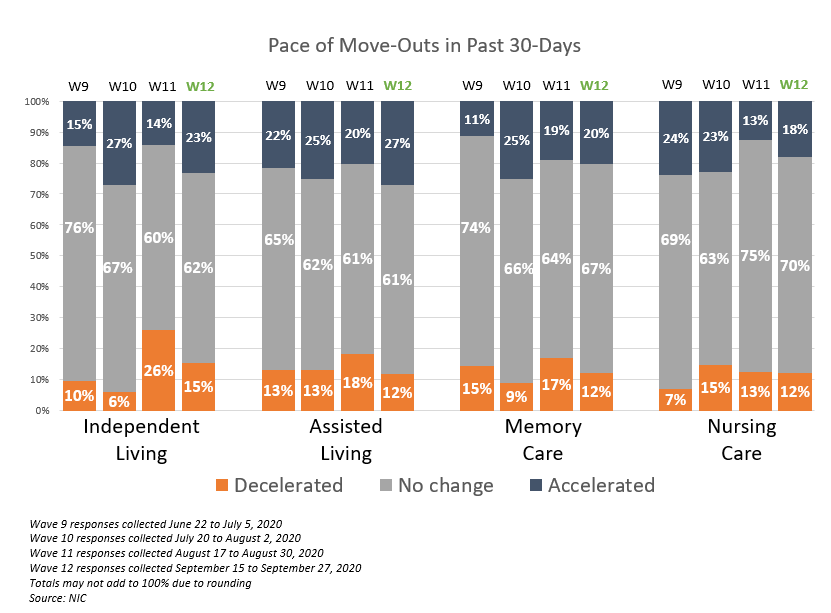

Pace of Move-Ins and Move-Outs

Respondents were asked: “Considering my organization’s entire portfolio of properties, overall, the pace of move-ins and move-outs by care segment in the past 30-days has…”

- In Wave 12, more organizations with memory care units report an acceleration in the pace of move-ins than in any other wave of the survey (51%). However, for the independent living and assisted living care segments, the shares of organizations reporting acceleration in the pace of move-ins in Wave 12 of the survey remained similar to Wave 9 (surveyed late June/early July).

- The shares of organizations with nursing care beds reporting declines in the pace of move-ins increased from Wave 11, and organizations reporting accelerations in the pace of move-ins retreated to Wave 8 levels (surveyed late May/early June).

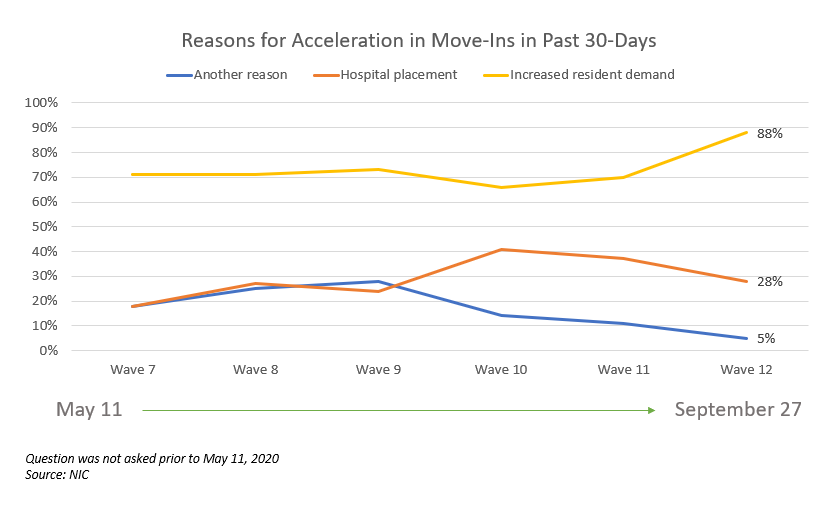

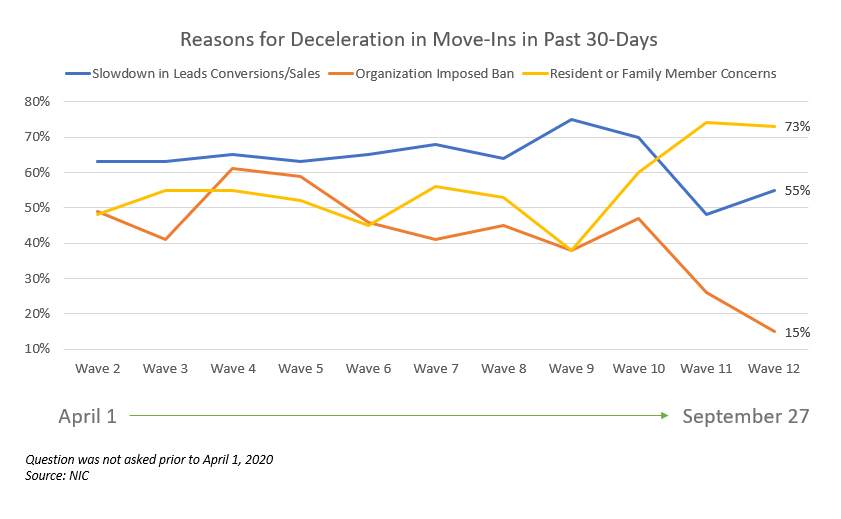

Reasons for Acceleration/Deceleration in Move-Ins

Respondents were asked: “The acceleration/deceleration in move-ins is due to…”

- The share of organizations citing increased resident demand as a reason for acceleration in move-ins is at the highest level since the question was asked in May (88%). Organizations citing hospital placement has declined since the peak reached in Wave 10, surveyed in the latter half of July (28% vs. 41%, respectively).

- Regarding reasons for a deceleration in move-ins, resident or family member concerns remained high (73%), and slightly more organizations in Wave 12 than in Wave 11 cited a slowdown in leads conversions/sales (55% vs. 48%). Organizations citing a moratorium on move-ins as reason for deceleration in the pace of move-ins is at the lowest level in the time series (15%).

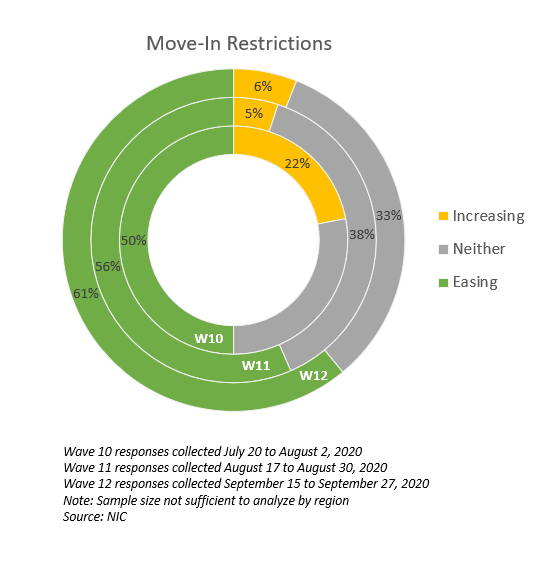

Organizations Easing or Increasing Move-In Restrictions

Respondents were asked to describe whether they were easing or increasing move-in restrictions in some or all of the geographies in which they operate.

- Roughly two-thirds (61%) of organizations were easing move-in restrictions in some or all of their geographies in Wave 12, compared to 56% in Wave 11 and 50% in Wave 10. One-third (33%) were neither increasing nor easing move-in restrictions in Wave 12.

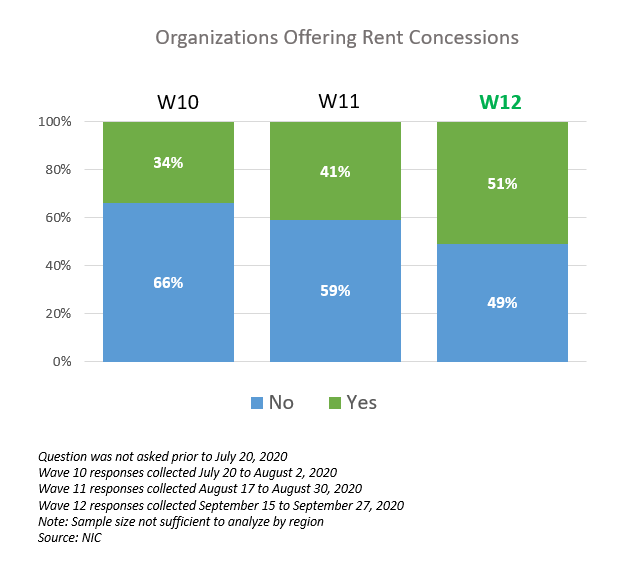

Organizations Currently Offering Rent Concessions to Attract New Residents and Organizations Experiencing a Backlog of Residents Waiting to Move-In

Respondents were asked: “My organization is currently offering rent concessions to attract new residents,” and “My organization is experiencing a backlog of residents waiting to move-in”

- The share of organizations offering rent concessions to attract new residents in Wave 12 has grown since Wave 10 from roughly one-third to one-half. Three-quarters of survey respondents indicate that their organizations do not currently have a backlog of residents waiting to move in.

Move-Outs

- The majority of organizations in Wave 12 of the survey continue to note no change in the pace of move-outs in the past 30-days. This has been consistent since the survey began in late March.

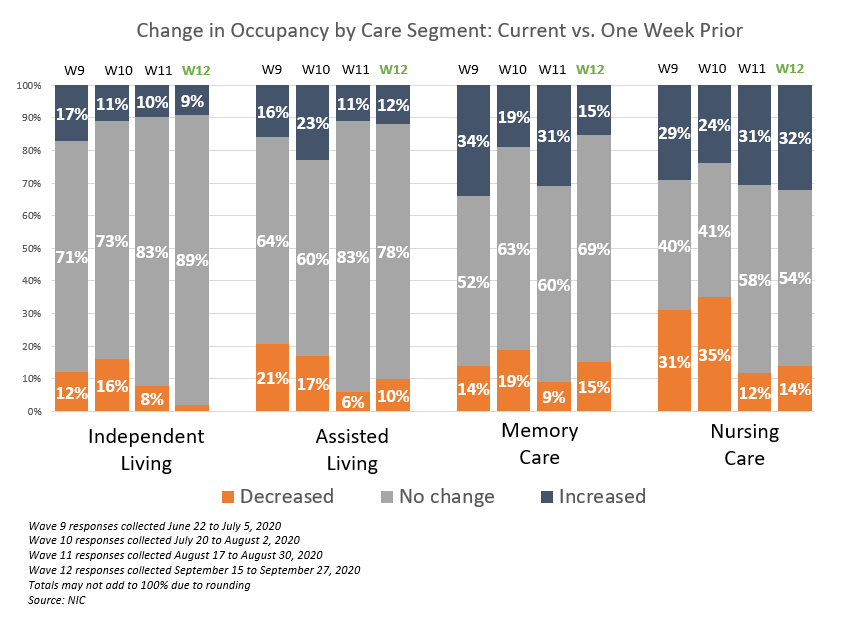

Change in Occupancy by Care Segment

Respondents were asked: “Considering the entire portfolio of properties, overall, my organization’s occupancy rates by care segment are… (Most Recent Occupancy, Occupancy One Month Ago, Occupancy One Week Ago, Percent 0-100)”

- In Wave 12, roughly one-third of organizations with memory care units report an increase in occupancy rates from one month prior, down from 40% in Wave 11, but higher than independent living and assisted living.

- The shares of organizations with independent living units and nursing care beds that report no change or increasing occupancy remain similar to recent waves of the survey. However, roughly half of organizations with assisted living units reported downward changes in occupancy rates in Wave 12.

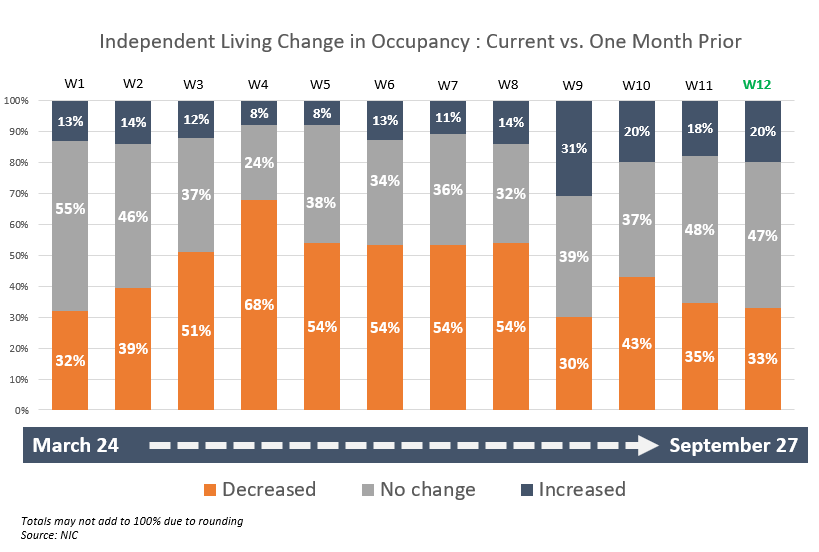

- The chart below shows the entire time series of independent living care segment month-over-month occupancy change data for each wave of the survey between March 24 and September 27, 2020.

- In Wave 4 of the survey (responses collected April 20-April 26, 2020) two-thirds of organizations reported occupancy declines from one month prior (68%). Occupancy rates began to improve in Wave 9 (responses collected June 22-July 5, 2020), with the largest shares of organizations reporting increases in occupancy in Wave 9 than at any other time during the survey (31%).

- In Waves 11 and 12, the largest shares of organizations with independent living report no change in month-over-month occupancy (48% and 47%, respectively) since Wave 2 of the survey.

- Regarding the change in occupancy from one week ago—about nine out of ten organizations with independent living units report no change in week-over-week occupancy (89%). While about one-third of organizations with nursing care beds reported improving occupancy rates (week-over-week) in both Waves 11 and 12, there has been more recent variability in the shares of organizations with memory care units reporting week-over-week changes in occupancy.

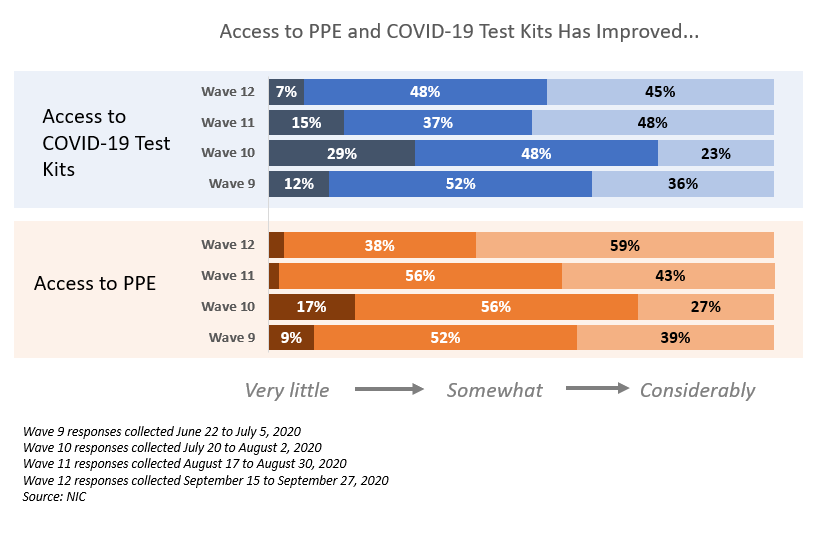

Improvement in Access to PPE and COVID-19 Testing Kits

Respondents were asked: “Considering access to PPE (personal protective equipment) and COVID-19 testing kits, my organization has experienced that access has improved... Very little, it is still difficult to obtain enough PPE/testing kits in most markets/Somewhat, in some markets it is easier to obtain PPE/testing kits than in others/Considerably, we typically have no difficulty obtaining PPE/testing kits, regardless of market”

- The availability of PPE and COVID-19 testing kits improved significantly in recent waves of the survey. In Wave 12, 59% report typically having no difficulty obtaining PPE, up from 27% in Wave 10. About half (48% and 45%, respectively in Waves 11 and 12) note considerable improvement in obtaining COVID-19 testing kits, up from 23% in Wave 10.

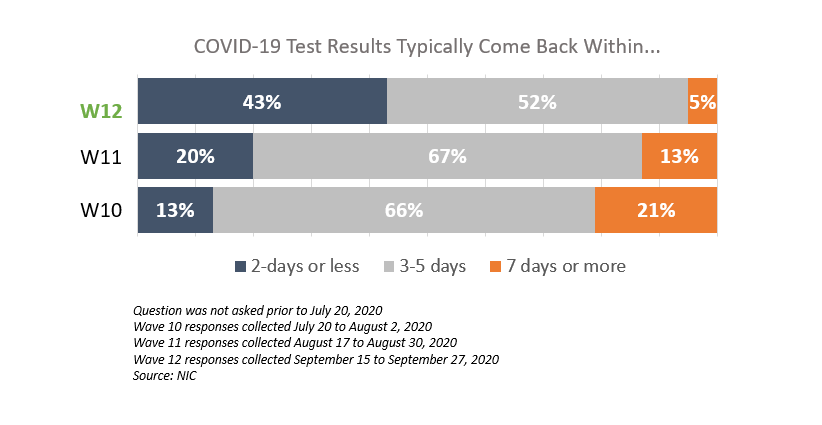

Time Frames for Receiving Back COVID-19 Test Results

Respondents were asked: “Regarding COVID-19 test results (either for staff, residents or prospective residents) results typically come back within…”

- The time frame for receiving COVID-19 test results has also improved significantly over prior waves of the survey. In Wave 12, 43% of organizations indicated their test results were being returned within 2 days. Nevertheless, the majority 57% note that it still takes more than 3 days to receive test results, however, this is up from 87% in Wave 10.

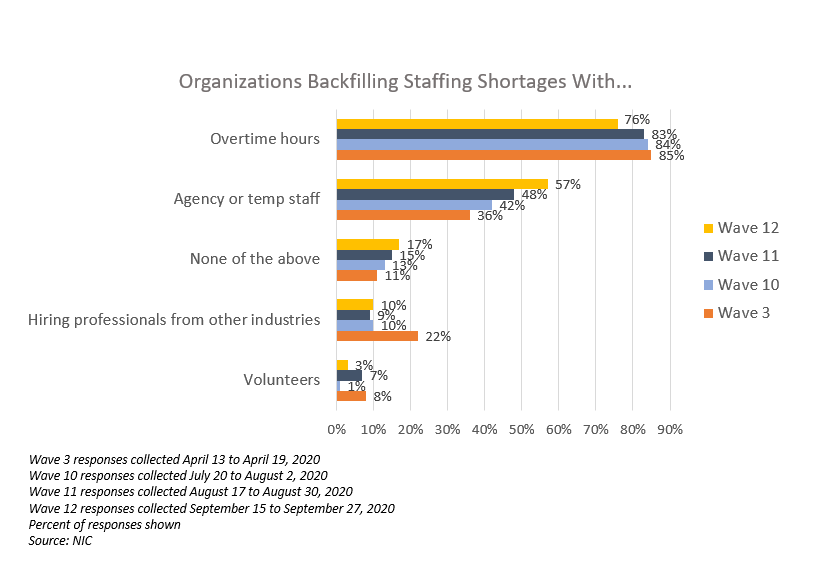

Labor and Staffing

Respondents were asked: “My organization is backfilling property staffing shortages by utilizing … (Choose all that apply).” Note: this question was asked in Wave 3, and then again in Waves 10-12.

- Organizations are increasingly using agency or temp staff to fill staffing vacancies. In Wave 12, more than half of respondents (57%) were tapping agency or temp staff to mitigate staffing shortages—up from 36% in Wave 3.

- Three-quarters are offering overtime hours in Wave 12 (down from 85% in Wave 3).

Owners and C-suite executives of seniors housing and care properties, we’re asking for your input! By providing real-time insights to the longest running pulse of the industry survey you can help ensure the narrative on the seniors housing and care sector is accurate. By demonstrating transparency, you can help build trust.

“…a closely watched Covid-19-related weekly survey of [ ] operators

conducted by the National Investment Center for Seniors Housing & Care…”

The Wall Street Journal | June 30, 2020

The Wave 13 survey is available until Sunday, October 11, and takes just 5 minutes to complete. If you are an owner or C-suite executive of seniors housing and care and have not received an email invitation to take the survey, please click this link or send a message to insight@nic.org to be added to the email distribution list.

NIC wishes to thank survey respondents for their valuable input and continuing support for this effort to bring clarity and transparency into market fundamentals in the seniors housing and care space at a time where trends are continuing to change.

About Lana Peck

Lana Peck, former senior principal at the National Investment Center for Seniors Housing & Care (NIC), is a seniors housing market intelligence research professional with expertise in voice of customer analytics, product pricing and development, market segmentation, and market feasibility studies including demand analyses of greenfield developments, expansions, repositionings, and acquisition projects across the nation. Prior to joining NIC, Lana worked as director of research responsible for designing and executing seniors housing research for both for-profit and nonprofit communities, systems and national senior living trade organizations. Lana’s prior experience also includes more than a decade as senior market research analyst with one of the largest senior living owner-operators in the country. She holds a Master of Science, Business Management, a Master of Family and Consumer Sciences, Gerontology, and a professional certificate in Real Estate Finance and Development from Massachusetts Institute of Technology (MIT).

Connect with Lana Peck

Read More by Lana Peck