Key Takeaways

- Occupied penetration rates in senior housing are changing across markets, likely due to shifts in demand dynamics and migration patterns.

- There is a trend of demand

and growth driven by the continuum of care, which could lead to improvements in occupied penetration rates for needs-based segments in the future.

- Seven markets are reporting their highest occupied penetration rates in 2023.

This analysis, conducted by NIC Analytics, explores the trends and variations in occupied penetration rates since 2017 across senior housing segments and markets within the 31 NIC MAP Primary Markets. It sets the foundation for an upcoming in-depth research segment within the NIC SHARK series. For purposes of this analysis, occupied penetration rates are defined as occupied senior living units relative to households aged 75+.

Occupied penetration rates in senior housing are changing across markets, likely due to shifts in demand dynamics and migration patterns. However, the overall penetration rate at the national level, known for its stability, remains a challenging puzzle to solve.

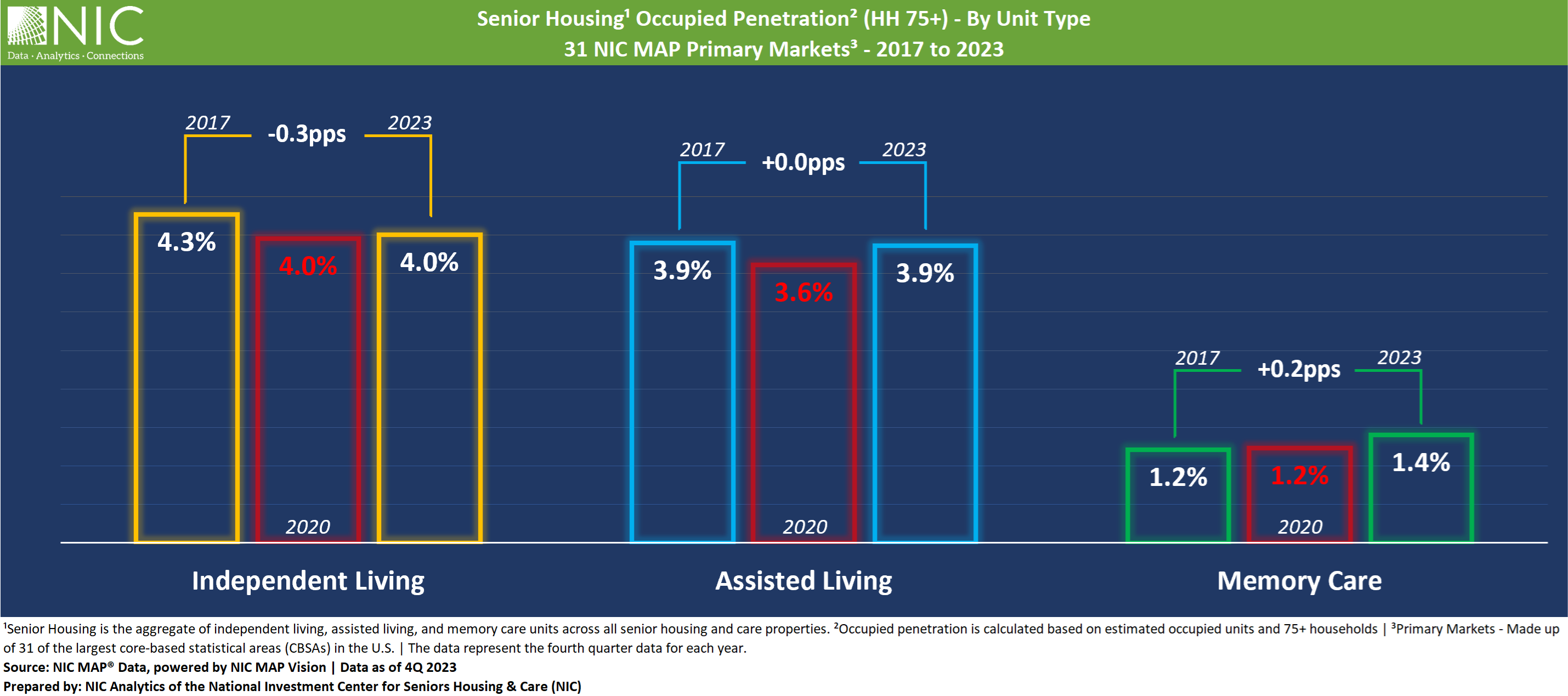

The exhibit below depicts the occupied penetration rates among households aged 75+ for senior housing units (independent living, assisted living, and memory care) across the 31 NIC MAP Primary Markets from 2017 to 2023.

Notably, there was a general decrease in occupied penetration rates across all unit types in 2020. By 2023, the occupied penetration rates for independent living fell below the 2017 levels. In contrast, the rates for assisted living remained stable, matching the 2017 levels, while the rates for memory care experienced a positive increase of 0.2pps, representing a 17% improvement over the last six years, from 1.2% to 1.4%.

In the last three years, we have observed a pattern where dynamics are shifting not only across markets but also among unit types. For instance, in terms of occupancy recovery and demand, memory care and assisted living units showed the earliest signs of recovery, despite having experienced the largest demand contraction, whereas independent living is lagging behind despite a relatively smaller demand contraction.

This observation prompts us to consider the continuum of care and its influence. It appears that there may be a trend of demand and growth driven by the continuum of care.

One plausible explanation for this trend could be tied to move-ins. In assisted living or memory care, residents typically fall into two categories: (1) those transitioning from independent living or assisted living, and (2) those coming from non-congregate settings. However, move-ins in independent living primarily originate from one source – non-congregate settings.

Additionally, when considering penetration rates—a metric that generally reflects preferences among older adults—distinguishing between those who prefer aging in a community versus those who opt for aging in place, assisted living and memory care have a distinct advantage. They are both considered needs-based, and services are often required.

The assisted living and memory care segments, being needs-based, already have a consumer pool of millions who have chosen to move to a senior housing setting and are currently part of the continuum of care. This existing consumer base is likely to contribute to improvements in occupied penetration rates for these segments in the future.

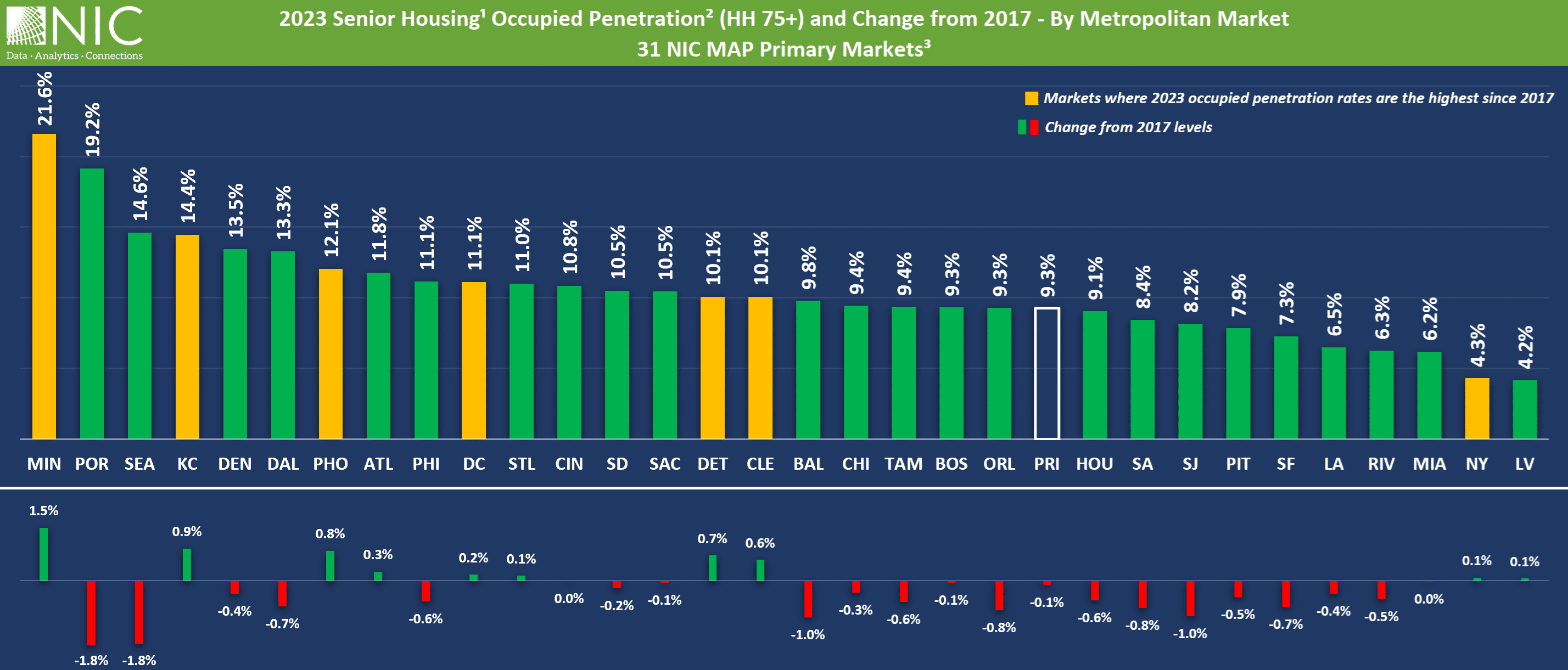

Occupied Penetration Rates in 2023: Market Trends and Variations

The exhibit below shows the 2023 senior housing occupied penetration rates and the change in percentage points from 2017 levels across all 31 NIC MAP Primary Markets.

There are notable variations in terms of these rates, with seven markets reporting the highest occupied penetration rates in 2023 since 2017. These markets include Minneapolis (21.6%), Kansas City (14.4%), Phoenix (12.1%), Washington, DC (11.1%), Detroit (10.1%), Cleveland (10.1%), and New York (4.3%).

Among the biggest gainers from 2017 to 2023 are Minneapolis, Kansas City, and Phoenix. Conversely, markets such as Portland, OR, Seattle, Baltimore, and San Jose experienced declines in occupied penetration rates between one and two percentage points.

The top markets with 2023 occupied penetration rates above the Primary Markets’ average of 9.3% include Minneapolis (21.6%), Portland (19.2%), Seattle (14.6%), Kansas City (14.4%), Denver (13.5%), and Dallas (13.3%). On the other hand, 10 markets fall below the Primary Markets’ average, with New York (4.3%) and Las Vegas (4.2%) ranking at the bottom.

These variations in occupied penetration rates may result from a variety of factors, including specific cultural differences in certain markets i.e., cultural views and financial support towards aging in place vs. aging in a community, which could be challenging to influence, or they could be tied to factors that are easier to impact. The upcoming research segment report will explore a multitude of factors and dive into the underlying drivers of high versus low senior housing occupied penetration rates in order to uncover hidden patterns and correlations at the market level and answer questions like:

- Why has the overall occupied penetration rate not shown notable changes over time?

- What factors contribute to higher occupied penetration rates in some markets and lower rates in others?

- Are there specific strategies that the senior housing sector can employ to positively impact occupied penetration rates?